Customer Profitability Case Interview: Segmentation Guide

Solve customer profitability case interviews: segmentation logic, cost-to-serve drivers, contribution margin, worked examples, questions, and practice drills.

On this page

A customer profitability case interview asks you to stop analyzing average company profit and identify which customer segments create or destroy value. The strongest approach is to segment customers by economic behavior, estimate revenue and cost-to-serve by segment, isolate the margin gap, then recommend whether the client should fix the service model, reprice the relationship, or exit only when the segment is structurally unattractive. Treat the prompt as a customer economics problem, not a generic revenue-minus-cost tree. Your issue tree should explain why a group is more valuable than another: order pattern, channel, product mix, customization, support load, returns, payment friction, and future value. If the client has growing sales but flat profit, or a large account that consumes unusual operational effort, move quickly from aggregate profit to contribution margin by segment. That is where the interviewer sees whether your structure actually explains the business.

If you need the broader revenue-cost tree before narrowing into segments, use the profitability case interview guide as the base layer.

What a customer profitability case is really testing

A standard profitability case asks why total profit changed. A product profitability case asks which product line earns attractive margin. A customer profitability case asks which customer, account, channel, or segment deserves management attention because its economics differ from the average.

That distinction matters because consulting interviews reward the way you structure a client problem. McKinsey frames interviews around problem solving in a client-like scenario, while Bain describes the case as a chance to work through an actual client problem with assumptions, quick math, and constructive reasoning. BCG also positions case preparation around showing how you think through consulting-style problems. None of that is about memorizing a tree; it is about choosing drivers that fit the prompt.

Listen for signals: sales are rising but profit is flat, a premium account is demanding, service cost is increasing, or growth from a channel feels less valuable than expected. Those prompts can look like a revenue decline case interview, but the answer lives in customer economics.

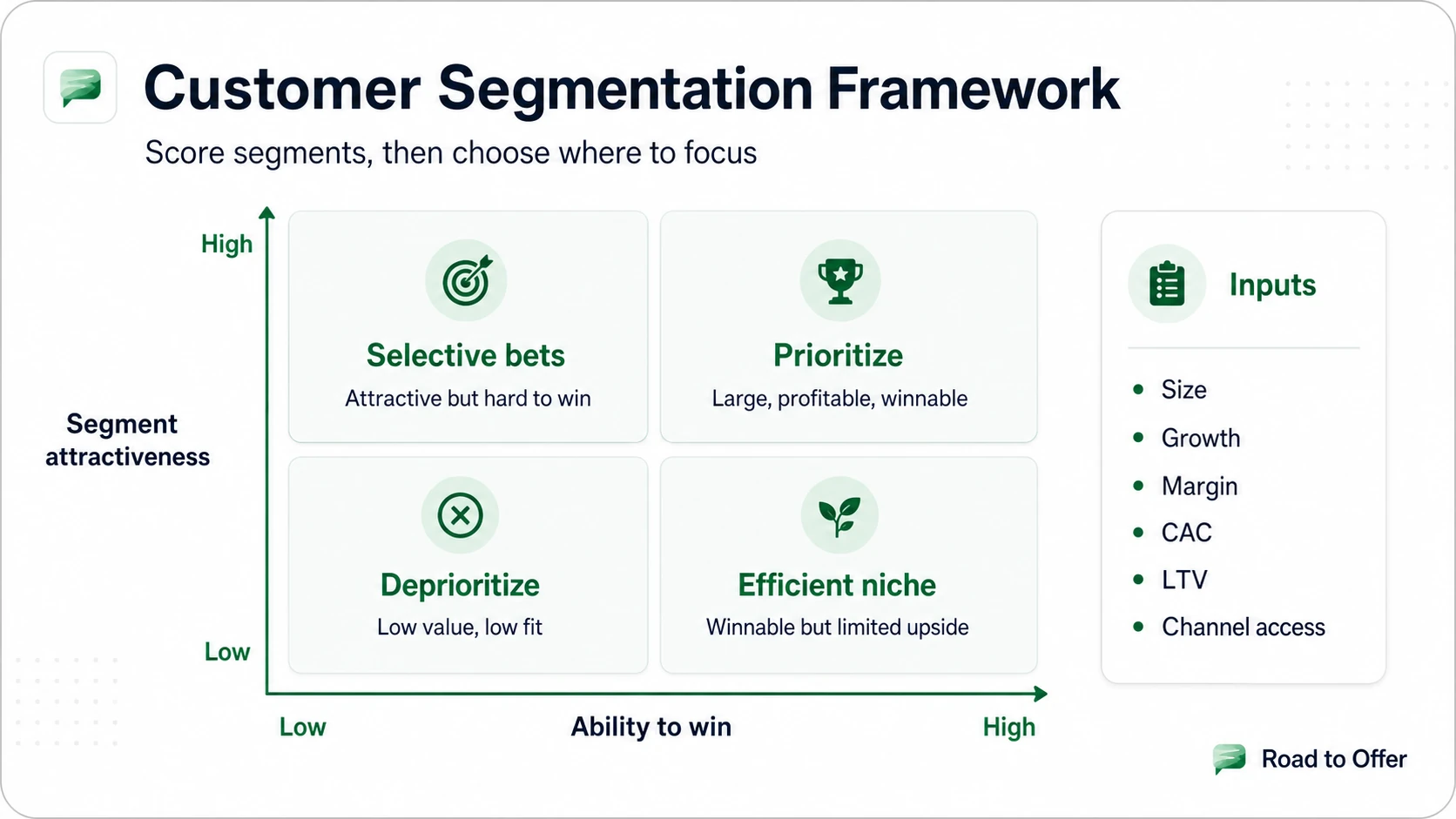

Segmentation table: choose cuts that explain margin

Segmentation is useful only when it explains revenue behavior, cost-to-serve behavior, or both. A driver tree helps because it forces each branch to answer a profit question rather than merely naming a customer type.

A superficial cut describes customers. A strong cut explains margin. If the segment label does not change revenue, variable costs, service activities, or customer lifetime value, it is probably a weak branch.

If you want to test whether this segmentation plan holds under pressure, Road to Offer helps by putting the issue tree, margin math, and final synthesis into a live free case practice.

Practice a customer profitability case

Work through a realistic Road to Offer case, then use the feedback to spot whether your segmentation, math, and synthesis hold under interview pressure.

Worked example: high revenue, weak margin

Imagine an industrial supplier whose leadership sees strong sales from enterprise accounts but weaker profit than expected. A generic profitability tree would split revenue and cost, then ask for price, volume, and major expense buckets. That is acceptable as a start, but it misses the likely issue: some customers may be buying a lot while also creating unusual delivery, support, and customization work.

A better candidate structure separates the case into customer segments, then asks how each segment behaves economically. Revenue branches might include account spend, discounting, product mix, and retention potential. Cost branches should include product cost, delivery complexity, rush handling, sales coverage, engineering changes, billing friction, and support time.

The segment comparison could show a standardized mid-market group with modest sales but clean orders, predictable delivery, and limited support. The enterprise group may have higher sales, but also custom terms, urgent requests, product changes, slower payment, and more senior account coverage. The diagnosis is not that high-revenue customers are bad. The diagnosis is that average accounting can hide customer-specific service cost.

Sample synthesis: the client should not exit large accounts immediately; it should separate accounts by customization and support intensity, test standard service tiers, and revise rush delivery or bespoke work terms before cutting relationships.

McKinsey

McKinseyProfitability · medium

Practice a full profitability case

Consumer Packaged Goods / Beverages

Questions to ask before you segment

Before segmenting, clarify the business objective. Is the client trying to improve near-term profit, protect strategic accounts, reduce operational load, or decide where to focus growth? The answer changes the segmentation logic.

Ask customer economics questions: Which customer groups drive revenue? Which receive discounts? Which buy higher-margin products? Which groups have better retention value? Use the customer lifetime value framework when the interviewer signals that current margin is not the whole story.

Ask cost questions: Which costs vary with order behavior? Which activities create delivery, customization, support, returns, disputes, or collections work? Which costs are truly customer-specific, and which are fixed costs that should not be blamed on a segment too quickly?

Ask data-quality questions before recommending exit. Do we have service activity by customer? Are costs allocated based on real behavior or broad averages? Could a channel change, minimum order rule, pricing tier, or operating redesign repair the economics?

Cost-to-serve and contribution margin math

The interview-safe formula is simple: segment contribution margin = segment revenue - direct product cost - customer-specific service cost. The hard part is deciding which costs belong in the customer view. Direct product cost belongs if it varies with the sale. Delivery, support, customization, returns, disputes, and sales coverage belong when they are caused by the customer relationship. Broad overhead should be handled carefully because spreading it evenly can punish the wrong segment.

Corporate Finance Institute explains customer profitability analysis as a way to evaluate customers or segments based on the activities and expenses involved in serving them. Harvard Business School Faculty & Research also lists Kaplan and Narayanan's work on measuring and managing customer profitability, which reinforces the point that this is a management accounting lens, not a case-interview trick.

In the case, translate activity-based costing into plain language. Ask which activities each segment consumes, then assign costs to those activities where the interviewer gives data. Do not average support time across all customers if the prompt says a certain group needs more help. Do not treat fixed costs as a reason to exit a segment unless the cost actually changes when the customer behavior changes. For more practice connecting revenue, cost, and margin at the customer level, the unit economics framework is the right companion article.

Recommendation checklist: fix, reprice, or exit

The final answer should compare fix, reprice, and exit. Weak answers jump from low margin to fire the customer. Strong answers ask whether the economics can be repaired without destroying strategic value.

Fix the service model when the customer is valuable but the operating model is inefficient. Examples include moving small orders to self-service, setting clearer customization rules, reducing rush delivery, changing support coverage, or standardizing implementation.

Reprice when the customer wants a service level that the current price does not support. That can mean service tiers, minimum order terms, rush fees, revised discounting, or paid customization. The recommendation should explain customer reaction risk, not just profit impact.

Exit only when the segment is structurally unattractive after reasonable fixes. Before doing that, check strategic value, referrals, future expansion, channel access, and retention value. A useful Synthesis drill should force you to state the action, the reason, the risk, and the next test in the same answer.

Practice drill path for customer profitability cases

Road to Offer works best here when you split the skill into parts instead of repeating full cases with the same weak link.

Start with structure. Use the Case interview structure drill to build a customer segment issue tree that separates revenue behavior from cost-to-serve behavior. Then review the profitability framework to make sure your tree still connects back to revenue, cost, and margin.

Next, practice math. Use Case interview math practice for contribution margin, segment comparison, and activity cost allocation. Then practice the final answer with the Synthesis drill, because customer profitability cases are won or lost when you turn the segment diagnosis into a fix, reprice, or exit recommendation.

Use the targeted drills when you know the weak skill and want targeted reps before another full case. The goal is not to memorize a customer profitability script. The goal is to build a repeatable habit: segment by economics, calculate the right margin, diagnose cost-to-serve, and recommend the least risky profitable action.

When you know which link is weak, Road to Offer drills let you repair that specific part instead of repeating full cases and hoping the pattern fixes itself. For adjacent archetype cases: the profitability case interview guide is the parent framework when customer profitability is a branch inside a broader margin case. The revenue decline case interview applies when the customer profitability issue is driving top-line decline. The cost reduction case interview covers the cost-to-serve reduction options once the unprofitable segments are identified. The pricing strategy case interview is the repricing lever once you know which segments are underpriced. The scale vs. profitability case interview addresses the strategic question of whether to grow the customer base or tighten it.

Practice a full customer profitability case

Run a full Road to Offer case so customer segmentation, profitability math, and synthesis hold together under interview pressure.

Sources and Further Reading (checked 2026-06-03)

- McKinsey & Company - Interviewing at McKinsey

- Bain & Company - Interviewing

- Boston Consulting Group - Consulting Case Study Interview Preparation

- Corporate Finance Institute - Customer Profitability Analysis

- Harvard Business School Faculty & Research - Measuring and Managing Customer Profitability

- Federal Reserve Bank of Kansas City - Customer Profitability Analysis Part I: Alternative Approaches Toward Customer Profitability

Frequently asked questions

Resources and related guides

- Start free consulting drillsPractice

- Browse all free resourcesResource hub

- Unit Economics Framework for Case InterviewsFrameworks · Jun 1, 2026

- Case Structure vs Case FrameworkFrameworks · May 1, 2026

- Cost Reduction Case Interview: Framework, Worked Examples, and Common Traps (2026)Frameworks · Mar 20, 2026

- Retail Case Interview: Framework, Omnichannel Strategy, and Worked Examples (2026)Frameworks · Mar 25, 2026