Unit Economics Framework for Case Interviews

Learn how to use the unit economics framework in case interviews, with branch questions, a worked EV charging example, mistakes, and a practice drill path.

On this page

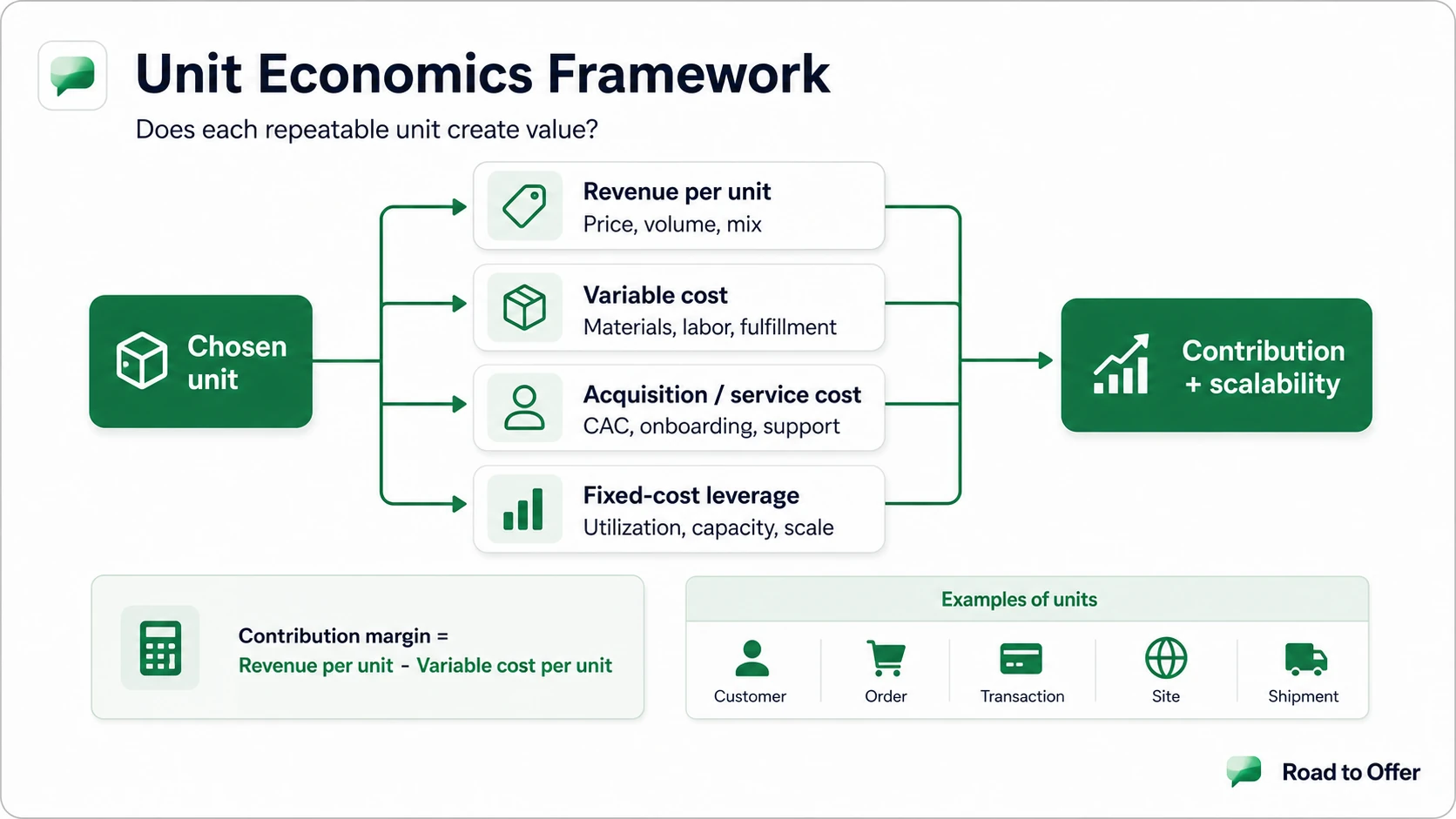

A unit economics framework breaks a business problem into the profit and cash logic of a repeatable unit: a customer, order, subscription, store, charging session, shipment, seat, transaction, or product line. In a case interview, it is most useful when the client question depends on whether growth is attractive, pricing works, acquisition spend is justified, or scale will improve margin. The move is to define the right unit, calculate revenue and variable cost around that unit, connect acquisition or service cost where it matters, test fixed-cost leverage and utilization, then recommend what should change. Used well, unit economics turns a vague profitability case into a clear driver tree. Used badly, it becomes another memorized framework label.

If you want the broader diagnostic first, start with the profitability case interview guide, then come back to this page for the per-unit lens. The case interview frameworks complete guide shows how unit economics fits as a precision tool alongside the profitability framework, cost reduction, and driver tree. For subscription or retention-heavy businesses, the customer lifetime value framework extends unit economics to include acquisition cost, churn, and long-run margin across the customer relationship. When the per-unit economics feed a market-entry or growth decision, the market attractiveness framework and pricing strategy framework are the natural follow-on structures.

What the unit economics framework actually answers

The unit economics framework answers a specific question: does each repeatable unit create enough economic value to justify growth, pricing changes, investment, or operational fixes?

That unit depends on the business. In SaaS, it may be a customer account. In retail, it may be an order or store visit. In a marketplace, it may be a transaction. In manufacturing, it may be a product. In logistics, it may be a shipment. In an asset-heavy case, it may be a site, room, truck, flight, or charging session.

This lens is stronger than a generic profitability framework when the case is really about repeatability. A client asking whether to enter a new city, discount to win more customers, open more sites, reduce churn, or acquire users more aggressively is usually asking whether the next unit of growth is attractive. Paddle describes unit economics as tying revenue and cost to a chosen unit, which is the same logic you need in a case, even when the business is not software (Paddle).

It is the wrong tool when the problem is mainly portfolio strategy, brand positioning, regulatory risk, or a one-time investment decision with no repeatable unit. In those cases, use a broader driver tree or market structure first, then bring in unit economics only if a repeatable unit becomes decisive.

Unit economics table: the branches to test

A case-ready unit economics structure should look like a table of decisions, not a list of formulas. The branch order depends on the prompt, but the core branches are stable.

OpenStax frames breakeven and cost-volume-profit logic around selling price, variable cost, fixed cost, volume, contribution margin, and assumptions, which is why those branches matter in case math (OpenStax). If fixed cost and contribution margin are central, use a breakeven calculator to practice the setup before doing it live in an interview.

The branch-selection rule is simple: start where the client decision is most exposed. Growth points to unit revenue, variable cost, and acquisition cost. A new site or market entry points to utilization, capacity, and fixed-cost leverage. Pricing points to revenue per unit, demand response, and contribution margin.

Worked example: EV charging hub profitability

Imagine the client operates EV charging hubs and wants to know why profitability is weaker than expected. The unit should probably be a charging session, because that is the repeatable event where revenue, electricity cost, maintenance, and utilization meet.

A strong opening structure could sound like this: I would start by checking economics per charging session, then separate site-level costs and utilization. First, revenue per session: price paid, session length, discounting, and customer mix. Second, variable cost per session: electricity, payment processing, maintenance tied to use, and any service cost. Third, site economics: lease, equipment, labor, uptime, and capacity. Finally, I would test whether fleet discounts or low utilization are pulling contribution margin below what the site needs to cover fixed costs.

The data requests are practical. Ask for average price per session, electricity cost per session, maintenance cost tied to charger usage, site lease and labor, number of sessions by time of day, charger uptime, and the share of discounted fleet customers. Do not average everything into one fake cost per session too early. A site with healthy variable margin can still fail if utilization is weak. A full site can still fail if fleet discounts destroy contribution margin.

The final recommendation could be directionally clear: expand only in locations where charging-session contribution margin is positive and utilization is high enough to cover site fixed costs; pause weaker sites until pricing, uptime, or customer mix improves. Road to Offer is useful here because the same logic can be tested in free case practice, where the framework has to survive the prompt, the math, and the final recommendation.

If you want to test whether this prep plan works under pressure, Road to Offer helps by turning the table into targeted reps: define the unit, run the math, then synthesize the business action.

Drill unit economics under case pressure

Practice the structure, math, breakeven, and synthesis moves that make this framework useful in an actual case interview.

Questions to ask before choosing the first branch

The fastest way to weaken a unit economics case is to pick a unit before understanding the client decision. Ask a few clarifying questions, then build the structure.

What does the business consider one unit? If the answer is customer, think subscription revenue, retention, service cost, customer acquisition cost, and customer lifetime value. If the answer is order, think ticket size, fulfillment, labor, returns, and repeat purchase. If the answer is transaction, think take rate, payment cost, support, and marketplace balance. If the answer is site, think capacity, utilization, fixed cost, and local demand.

Is the issue margin, growth, pricing, or viability? A margin case points to revenue per unit and variable cost. A growth case points to acquisition cost, repeat behavior, and whether new units look like old ones. A pricing case points to demand response, discounting, and contribution margin. A viability case points to breakeven and fixed-cost coverage.

Which costs truly vary with each unit? Ingredient cost, electricity, payment processing, packaging, and shipment cost usually move with volume. Lease, salaried management, equipment, and platform build are fixed or step-fixed. This distinction matters because contribution margin is not the same as full profit.

Does the customer repeat? In SaaS and subscription cases, recurring revenue and retention may justify acquisition spend. In a coffee shop or food delivery case, repeat behavior still matters, but the unit may remain an order or store visit. In an asset-heavy business, repeat customers may matter less than utilization and capacity.

These questions also keep the framework custom. That matters because official case interview guidance from BCG emphasizes realistic business problems and problem solving, not framework recital (BCG). If you need a deeper distinction, read case structure vs case framework.

Common misuse patterns in case interviews

The first misuse pattern is forcing LTV/CAC into every case. Customer acquisition cost and customer lifetime value are helpful when the unit is a customer or account, especially in recurring-revenue businesses, but they distract in a factory, logistics, retail order, or charging-session case unless acquisition spend is actually driving the decision. Fix it by asking whether the client buys customers, transactions, or capacity.

The second mistake is hiding fixed costs inside a clean per-unit average. That can make an underutilized site look permanently bad or a high-volume site look healthier than it really is. Fix it by separating contribution margin from fixed-cost coverage and asking whether capacity is constrained.

The third mistake is ignoring utilization. In asset-heavy cases, the same site, charger, restaurant kitchen, aircraft, hotel room, or delivery fleet can look excellent or terrible depending on use. Fix it by asking what happens at peak demand, idle time, and realistic capacity.

The fourth mistake is mixing customer and transaction units. A marketplace candidate might calculate revenue per customer, cost per order, and retention by account in the same tree. That makes the math hard to follow and the conclusion weak. Fix it by choosing the main unit, then translating other metrics back into that unit.

The fifth mistake is treating contribution margin as full profit. Contribution margin tells you what is left after variable cost. It does not prove the business is profitable after fixed cost, acquisition, support, and capacity constraints. Fix it by stating what the metric proves and what still needs validation.

The last mistake is doing math without a recommendation implication. A number is only useful if it changes the answer: grow, raise price, reduce cost, improve utilization, renegotiate discounts, or stop scaling. For more finance-case context, use the finance case interview guide.

Practice drill: structure, math, breakeven, synthesis

Practice unit economics in the same order the case will test it. Start with Case interview structure drill: define the unit, choose the first branch, and explain why that branch matters. Then move to Case interview math practice: set up contribution margin, acquisition cost allocation, breakeven, and sensitivity without burying the recommendation.

Next, use the breakeven calculator when fixed cost and contribution margin determine whether the model works. If the case involves growth over time, use the CAGR calculator to keep the growth logic clean. Finish with the Synthesis drill, because the interviewer needs to hear what the client should do.

Then pressure-test the same contribution-margin and breakeven logic on a full profitability case where unit economics decide the recommendation.

Profitability · easy

Practice a unit-economics profitability case

CPG / Packaged Snacks

Road to Offer pulls these reps together in the Road to Offer drill engine, but the fastest path for this specific framework is targeted practice: math drills, structure first, breakeven second, synthesis last. McKinsey also points candidates toward business-case preparation and practice cases, which is a useful reminder that reading a framework is only the start (McKinsey).

How to turn the framework into a final recommendation

A strong recommendation has a clear order. State whether the unit economics are healthy. Name the limiting branch. Explain the action. Flag the risk to validate.

For the EV charging example, the close might sound like this: I would not expand all sites yet. The charging-session economics appear attractive only where utilization is strong and discounting is limited. I would prioritize sites with high uptime and healthy session contribution, renegotiate fleet discounts where they dilute margin, and pause expansion in lower-use locations until demand or pricing improves.

That answer works because it connects the math to a decision. It does not say unit economics are good in the abstract.

Use the same close in market-entry, pricing, SaaS growth, retail, and operations cases. If the unit is healthy and scalable, recommend growth with the biggest risk named.

After targeted drills, the next useful step is to run the whole case and see whether your structure, math, and synthesis stay connected.

Test the framework in a full case

Run one free Road to Offer case and see whether your unit economics logic survives the prompt, math, exhibits, and final recommendation.

Sources and Further Reading (checked 2026-06-01)

- McKinsey & Company - Interviewing

- Boston Consulting Group - Consulting Case Study Interview Preparation

- Yale Office of Career Strategy - Consulting

- Paddle - What are unit economics in SaaS?

- Paddle - Formula to calculate & reduce customer acquisition cost (CAC)

- Paddle - Customer lifetime value: Calculation, formula & SaaS business strategies for improving

- OpenStax - Calculate a Break-Even Point in Units and Dollars

- Shopify - Master the Break Even Analysis: The Ultimate Guide

Frequently asked questions

Resources and related guides

- Start free consulting drillsPractice

- Browse all free resourcesResource hub

- Ansoff Matrix vs BCG Matrix for Case InterviewsFrameworks · Jun 2, 2026

- Cost-Benefit Analysis Framework for Case InterviewsFrameworks · Jun 1, 2026

- Cost Reduction Case Interview: Framework, Worked Examples, and Common Traps (2026)Frameworks · Mar 20, 2026

- Customer Profitability Case Interview: Segmentation GuideFrameworks · Jun 3, 2026