NPV and Discounting in Case Interviews: The Shortcut-First Guide (2026)

How to handle NPV and discounting in case interviews fast: the perpetuity shortcut, the 10% default rate, no-calculator mental math, and exactly what to say out loud.

On this page

NPV and discounting in case interviews come up more often than candidates expect in 2026, and the good news is you almost never have to grind through textbook year-by-year math under pressure. The single highest-leverage move is the perpetuity shortcut: when cash flows are roughly constant and run for many years, present value is just cash flow divided by the discount rate. PrepLounge shows this directly, where a constant 100 per year at a 4% discount rate is worth 2,500 today (100 / 0.04). When no rate is given, default to 10%. Interviewers are not grading whether you can recite a financial-modeling formula. They grade three things: whether your math is fast and accurate, whether your reasoning is structured, and whether you land on a crisp business recommendation. This guide gives you the exact moves and the words to say, so you can pick a rate, run the division, and recommend in under a minute.

What NPV actually is (and the intuition that makes it click)

Start with the gut-level question, not the formula: would you rather have $100 today or $100 a year from now? Everyone takes the money today. You could invest it, prices might rise, and a promise of future cash carries risk. That preference is the whole idea behind net present value. A dollar today beats a dollar tomorrow, so any future cash has to be marked down, or discounted, before you can compare it to money you hold right now.

Net present value takes every future cash flow a project will throw off, discounts each one back to today's value, adds them up, and subtracts the upfront investment. If the total is positive, the project creates value. If it is negative, it destroys value. That is it. The formula looks intimidating, but the intuition is just "future money is worth less, so shrink it before you trust it." Hold onto that picture, because the rest of this guide is about doing the shrinking quickly and saying the right thing while you do.

Practice NPV cases with instant AI feedback

Run a free case and get scored on your math speed, structure, and recommendation, the three things interviewers actually grade.

The NPV formula and how discounting works mechanically

The mechanical formula is short. The present value of a single cash flow is:

PV = CF / (1 + r)^n

where CF is the cash flow, r is the discount rate, and n is the number of years until you receive it. You compute that for each year, sum them, and subtract the upfront investment to get NPV.

A worked example from CaseBasix shows the full grind: a $200,000 investment that generates $60,000 per year for five years at a 10% discount rate. You discount each year and sum, NPV = (60,000 / 1.1) + (60,000 / 1.1^2) + ... + (60,000 / 1.1^5) minus 200,000. The fast way to verify the sum: the five-year annuity factor at 10% is 3.7908 (it is just those five discount factors added together, 0.909 + 0.826 + 0.751 + 0.683 + 0.621). So the present value of the five cash flows is 60,000 × 3.7908 = about $227,448, and subtracting the $200,000 outlay leaves an NPV of about $27,448. PrepLounge runs the same line-by-line logic on a smaller stream: 102 received in year one at a 2% rate is worth 100, 102 in year two is worth 98.04, and the combined present value is 198.04.

Notice how much arithmetic that is for two or five years. Now imagine ten or twenty years. That is exactly why the next section matters: in a live case you want to avoid this grind whenever the cash flows let you. The full discount-and-sum is the right tool only for short, uneven streams. For everything else, there is a shortcut. For the broader toolkit of formulas you should have memorized, keep the case interview formulas guide open alongside this one.

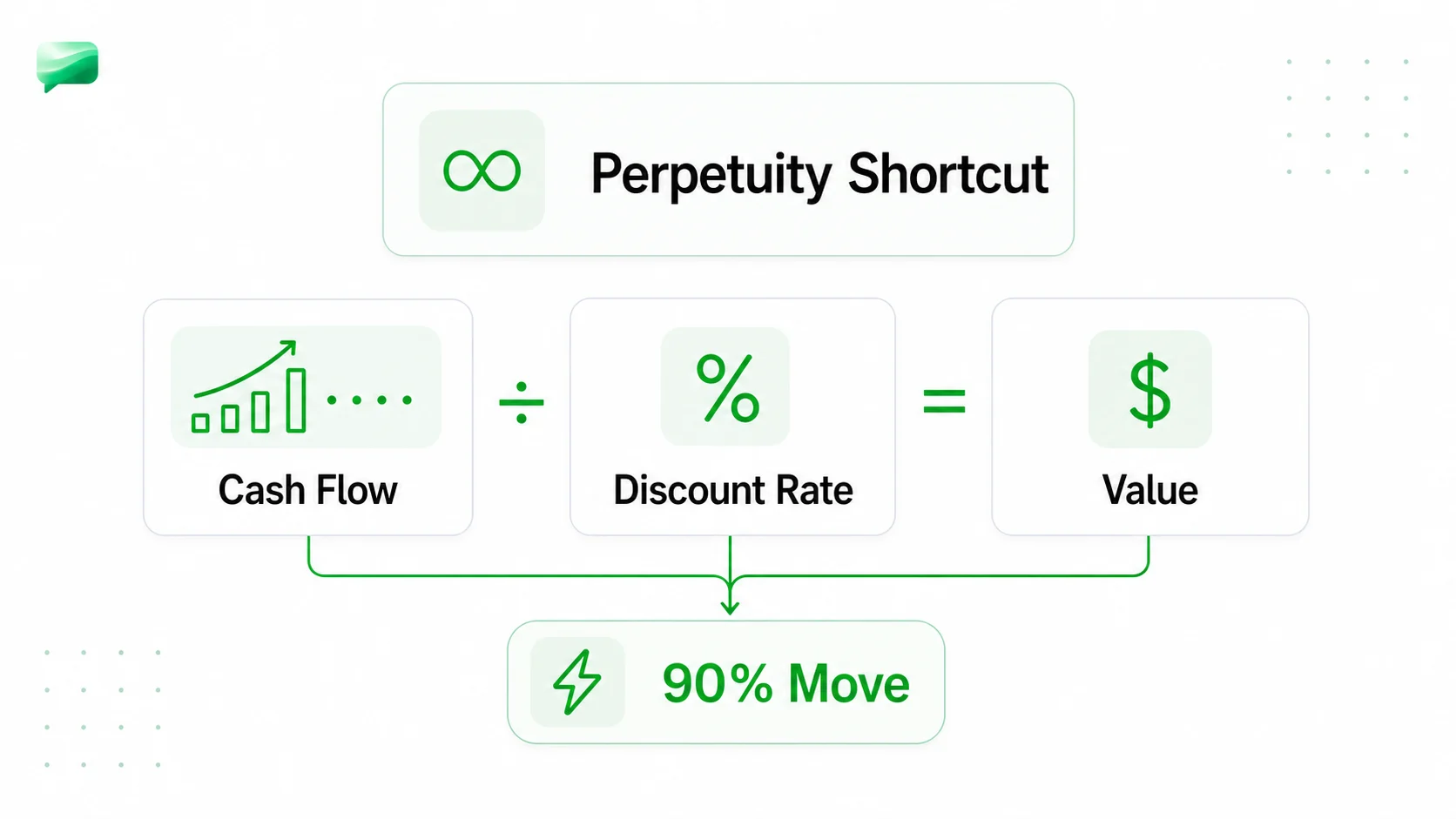

The perpetuity shortcut: your 90% move

Here is the move that wins most NPV cases. When cash flows are roughly constant and continue for many years, present value collapses to a single division:

PV = CF / r

That is the perpetuity formula, and it is the most useful thing in this entire guide. PrepLounge demonstrates it cleanly: a constant 100 per year at a 4% discount rate is worth 2,500 (100 / 0.04). CaseBasix does the same with bigger numbers: $10,000 per year indefinitely at a 5% rate is worth $200,000 (10,000 / 0.05). The same logic gives you instant intuition on round numbers, so $5 million a year at a 10% rate is worth $50 million, which you can say out loud the moment you see the cash flow.

The reason this works: discounting an infinite, level stream mathematically converges, and all those fractions sum to the clean ratio CF / r. In a case, the cash flows are never truly infinite, but "constant for many years" is close enough that the shortcut gives you a fast, defensible estimate. You trade a tiny bit of precision for a massive speed gain, and interviewers reward that judgment.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

The growing-perpetuity variant

If the cash stream grows at a steady rate, extend the shortcut to the growing-perpetuity (Gordon growth) form:

PV = CF / (r - g)

where g is the annual growth rate. PrepLounge's example: 100 per year growing at 2% with a 4% discount rate is 100 / (0.04 - 0.02) = 5,000. Notice the growth doubled the value versus the flat perpetuity, because you are subtracting a smaller number in the denominator.

The hard rule, and a classic trap: g must stay below r. If growth reaches or exceeds the discount rate, the denominator hits zero or goes negative and the formula produces nonsense (an infinite or negative value). If a case hands you a growth rate near your discount rate, that is a signal to either pick a higher rate with a stated reason or treat the stream as finite instead.

Choosing and justifying the discount rate (without doing CAPM in your head)

Candidates lose more time here than anywhere else. You do not need a precise weighted average cost of capital. You need a defensible rate and one sentence to justify it.

The default: when no rate is given, use 10%. Both PrepLounge and ConsultingBootcamp land on 10% as the "when in doubt" rate because it roughly reflects long-term market returns. From there, adjust by risk:

MyConsultingCoach frames it as a spectrum from roughly 3% for a very safe business to 20% for a very risky venture, while PrepLounge notes speculative start-ups can justify rates as high as 40%.

How much WACC do you actually need? Just enough to sound credible. ConsultingBootcamp walks through a Starbucks example with a risk-free rate of 3%, a beta of 0.8, and a market return of 8%, arriving at a WACC of 6.3%. That is a fine illustration of the machinery, but you should not run CAPM live. The pro move is to name a rate and justify it in one line: "I'll use 10% as a market-return baseline, and nudge it up because this is an early-stage bet." Then keep moving.

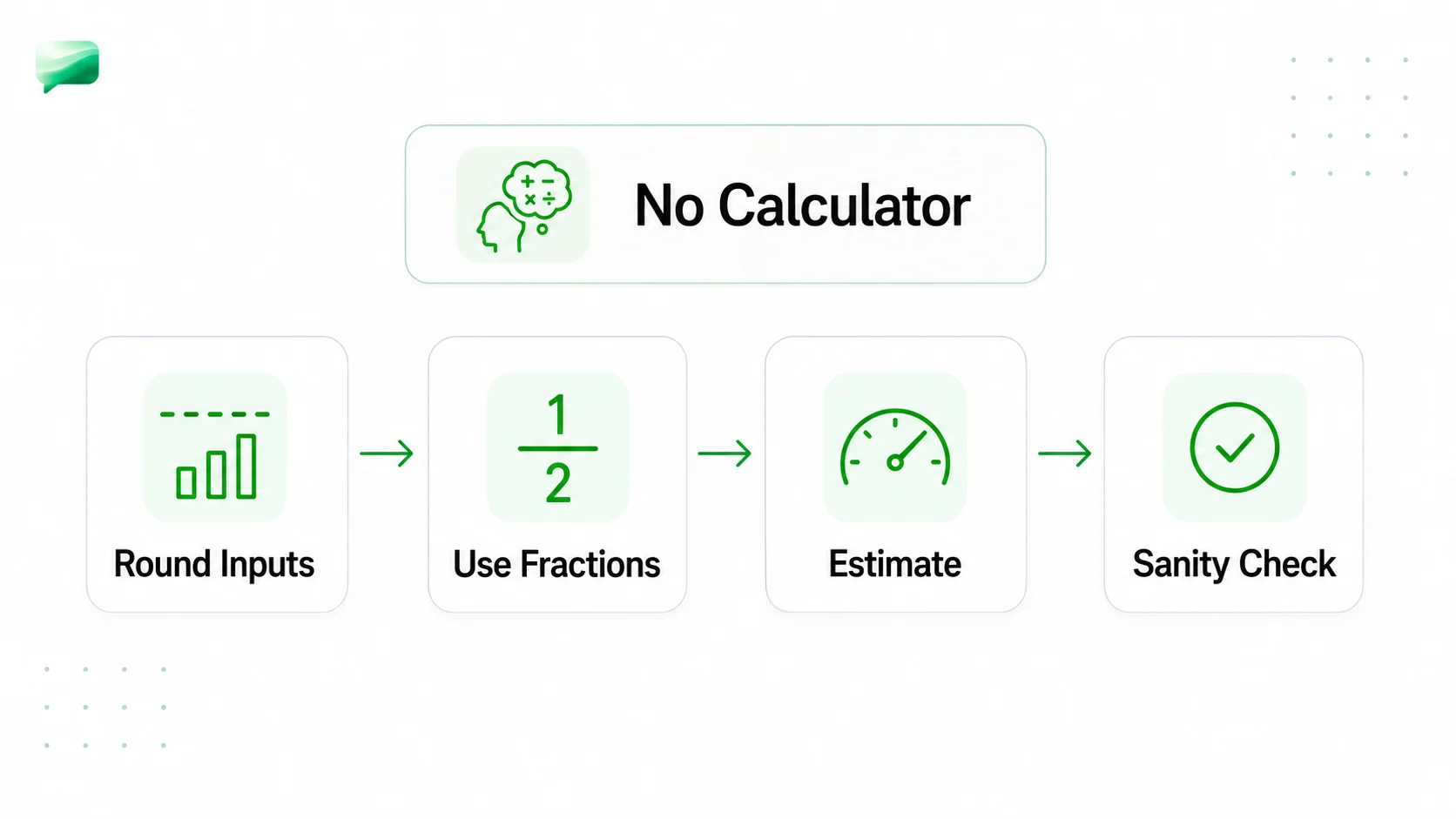

Doing the math without a calculator

Firms grade accuracy and efficiency together, so build a few habits that let you discount in your head.

- Lead with the perpetuity shortcut. CF / r is one division. Memorize the easy reciprocals: dividing by 10% means multiplying by 10, by 5% means multiplying by 20, by 8% means multiplying by 12.5.

- Round the rate to something clean. If the case says 9% or 11%, reason at 10% first to get the order of magnitude, then note "the true rate is slightly higher, so the real value is a touch lower." That sentence shows judgment without slowing you down.

- Use discount-factor approximations for short streams. Year one at 10% is about 0.91, year two about 0.83, year three about 0.75. Many candidates just use 0.9, 0.8, 0.7 to estimate fast, then flag the rounding.

- Anchor on round-number sanity checks. $5 million a year at 10% is $50 million. If your detailed math lands far from that anchor, you made an arithmetic slip.

If your mental arithmetic is the bottleneck, drill it deliberately before you touch a single case. The case interview math practice guide has timed sets for exactly this kind of division and rounding speed.

Interpreting the result and stress-testing the verdict

The verdict rule is simple: positive NPV means the project creates value, so do the deal; negative NPV means it destroys value, so walk away. But a good candidate never stops at the sign. You check how fragile that sign is.

The discount rate you picked can flip the answer entirely. ConsultingBootcamp shows a single project with an NPV of $154,612 at an 8% discount rate that flips to negative $7,898 at a 14% rate. Same cash flows, same project, opposite recommendation, purely because the rate moved six points.

That is why you say the rate out loud and explain your sensitivity: "At 10% this is clearly positive, but if the business is riskier than I assumed and the rate is closer to 14%, it becomes marginal. I'd want to confirm the risk profile before committing." That single sentence is often worth more than the exact NPV figure.

When NPV shows up versus payback period and ROI

NPV is not always the right tool. Treat it as one branch of a decision tree:

- Reach for NPV when the horizon is long, the cash flows are uneven or stretch over many years, or you are valuing an acquisition or comparing investments with different timing. MyConsultingCoach's valuation case, for instance, weighs an acquisition price of $1 million against an estimated valuation of $1.5 million, which is a clean NPV-style "is it worth more than it costs" question.

- Reach for payback period when the interviewer cares about how fast the cash comes back or about liquidity risk. It ignores the time value of money but answers "how long until we are whole" instantly.

- Reach for ROI when you want a quick percentage return and timing is not the crux.

In a real case you often run more than one. Use NPV for the value verdict, then a quick payback or ROI as a sanity check the interviewer can grasp in one breath. For the full comparison and when to deploy each, see the ROI and payback period case interview guide, and for the related "when does this investment turn cash-positive" question, the break-even analysis guide covers the companion calculation.

How to talk through your NPV answer out loud

The number is half the score. The communication is the other half. Use this four-beat script every time:

- State your assumptions. "I'll assume these cash flows are roughly constant for the foreseeable future, so I can treat them as a perpetuity."

- Pick a rate and justify it in one sentence. "With no rate given, I'll use 10% as a market baseline, adjusting up slightly for the risk in this business."

- Run the math out loud. "So that's roughly $5 million divided by 10%, which is about $50 million in present value, against an upfront cost of X."

- Recommend, then caveat. "That's clearly value-creating, so I'd do it. The main thing I'd pressure-test is the discount rate, because if risk pushes it toward 15% the case gets much tighter."

Saying it in that order signals structure before the interviewer even checks your arithmetic. It is the difference between a candidate who computed a number and one who made a decision.

Common traps and limitations

- Forgetting the initial investment. NPV is the present value of future cash flows minus the upfront cost. Compute a beautiful $50 million PV and forget to subtract the $40 million you spent, and your recommendation is wrong. Say "minus the upfront investment" out loud so you never skip it.

- Letting g reach or exceed r. In the growing-perpetuity formula, if growth meets or beats the discount rate, the math explodes. If a prompt nudges you there, switch to a finite horizon or a higher rate with a reason.

- Over-engineering the discount rate. Nobody wants you to derive beta and run CAPM live. The Starbucks WACC of 6.3% is a teaching illustration, not a live expectation. Name a rate, justify it in a sentence, move on.

- Ignoring synergies and terminal value in M&A. In acquisition cases, the value often lives in synergies and the long-tail terminal value, not just the next few years of standalone cash flow. Flag them even if you only estimate them roughly.

- Treating the answer as precise. NPV is only as good as your rate and your cash-flow assumptions. Present a range or a sensitivity, not a single deceptively exact figure.

Sources (checked June 26, 2026)

- PrepLounge, Net Present Value (NPV): https://www.preplounge.com/en/case-interview-basics/net-present-value-npv

- CaseBasix, Case Interview Formulas: https://www.casebasix.com/pages/case-interview-formulas

- MyConsultingCoach, Net Present Value: https://www.myconsultingcoach.com/news/net-present-value

- MyConsultingCoach, Case Interview Valuation: https://www.myconsultingcoach.com/case-interview-valuation

- ConsultingBootcamp, How to Find the Discount Rate in NPV Cases: https://consultingbootcamp.co/how-to-find-the-discount-rate-in-npv-cases-a-friendly-guide-for-the-perplexed/

Put the perpetuity shortcut to work

Run a free AI-guided case to practice picking a rate, running the math, and recommending out loud under real time pressure.

Frequently asked questions

Resources and related guides

- Try a full casePractice

- Browse all free resourcesResource hub

- Case Interview Formulas: Cheat Sheet for Profitability and Math (2026)Math And Quant · May 1, 2026

- Numerical Reasoning Test for Consulting (2026): Format, Question Types & How to PassMath And Quant · Jun 28, 2026

- Best Free AI for Case Interview Math Practice (2026)Math And Quant · May 8, 2026