Break-Even Analysis for Case Interviews: Formula, Worked Examples, and When to Use It (2026)

The complete break-even guide for case interviews: the formula, contribution margin, break-even price, margin of safety, and five fully worked numeric examples with the actual arithmetic and the sanity-check that wins offers.

On this page

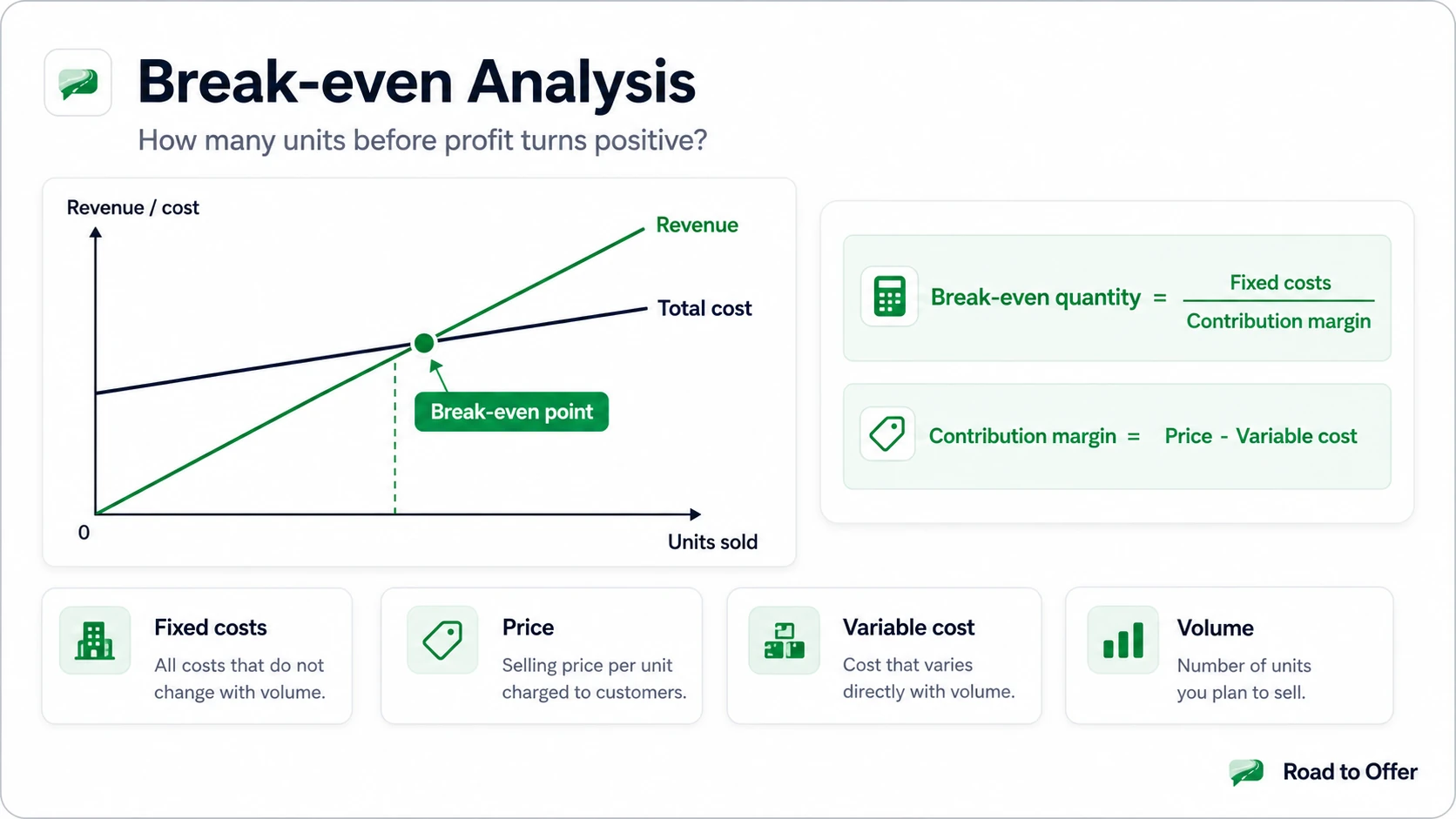

Break-even analysis in a 2026 case interview answers a single question: how many units must a company sell before revenue covers all costs and profit equals zero? The formula is Break-Even Quantity = Fixed Costs / (Price - Variable Cost per unit), where the denominator is the contribution margin, the amount each unit throws at fixed costs before it converts to profit. The arithmetic itself is easy: a wireless earbuds launch with $2,000,000 in fixed costs and a $24 contribution margin breaks even at roughly 83,000 units a year, well under 0.1% of the 100M-plus unit U.S. wireless earbuds market that Statista tracks annually, which is why the number alone rarely settles the case. What separates a strong candidate is correctly splitting fixed from variable costs, choosing the right variant of the formula for the question actually asked, and then judging whether the break-even volume is achievable against real market size, cost structure, and demand.

What Is the Break-Even Formula and Its Components?

The formula has three inputs and one derived term. Get the cost split right and the rest is division.

The intuition: each unit throws $40 at a $500,000 wall of fixed costs, so you need 12,500 units to knock it down, and unit 12,501 is the first dollar of profit. The mistake hiding in plain sight is dividing $500,000 by the $100 price for 5,000 units. That is wrong by 2.5x because it pretends every dollar of revenue covers fixed costs when $60 of it was already spent making the unit.

How Do You Split Fixed vs. Variable Costs?

Misclassifying costs is the error interviewers watch for most, because it quietly breaks the whole calculation. The trap they love is treating all labor as fixed. Salaried managers are fixed; hourly production workers who clock more hours as volume rises are variable.

When a cost is semi-variable, split it: the base charge is fixed, the per-unit usage is variable. Saying that out loud signals you understand cost behavior rather than memorizing buckets.

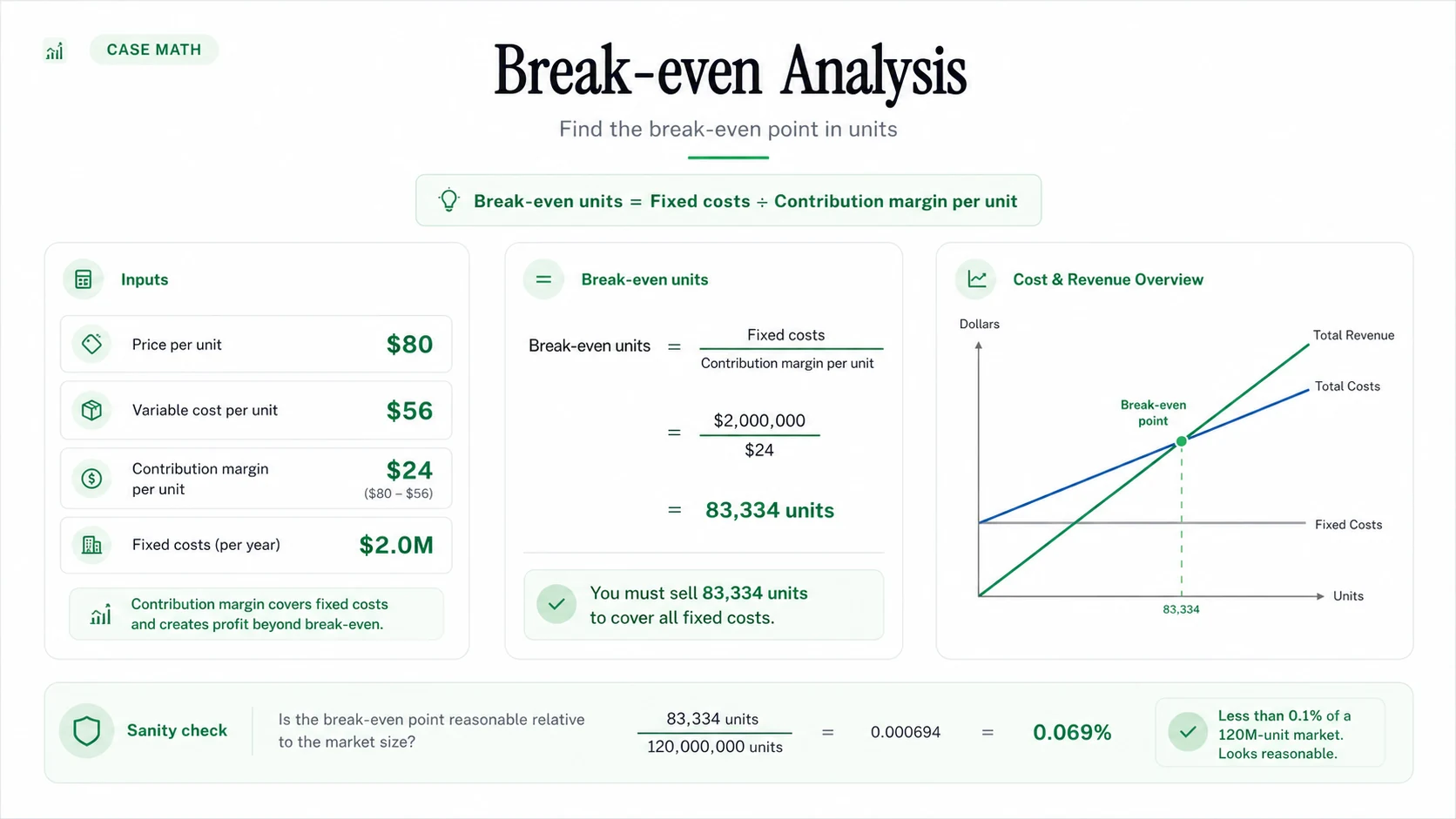

Worked Example 1: New Product Launch

Prompt: A consumer electronics company is considering launching wireless earbuds. How many units must it sell annually to break even?

Given data:

- R&D: $3M amortized over a 3-year product life = $1M/year; facility lease: $400K/year; staff: $600K/year

- Total fixed costs: $2,000,000/year

- Price: $80; components: $28; assembly: $7; packaging and shipping: $5; retailer margin: $16

- Total variable cost: $56/unit

Calculation:

- Contribution margin = $80 - $56 = $24/unit

- Break-even = $2,000,000 / $24 = 83,334 units/year (83,333.3 rounded up, since you cannot break even on a fractional unit)

Sanity check: The U.S. wireless earbuds market runs in the range of 100M+ units annually (Statista). At ~83,000 units the client needs well under 0.1% market share, which is realistic for an established brand. The break-even is achievable, so the constraint is demand and distribution, not the math.

Top-candidate addition: "If we negotiate the retailer margin from $16 to $12 per unit, variable cost drops to $52, contribution margin rises to $28, and break-even falls to $2,000,000 / $28 = 71,429 units, a 14% improvement. I'd also model a direct-to-consumer channel that captures the full margin."

Lock in the basic mechanics with three reps built directly from the earbuds numbers above.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

Practice break-even calculations from the Road to Offer drill engine: a real prompt, your answer, and AI-scored feedback. Free account includes free daily drills.

Worked Example 2: A Pricing Decision

Prompt: A B2B SaaS company has 2,000 customers paying $50K/year, with $12K variable cost per customer and $50M in fixed costs. It is considering dropping the price to $40K. How many customers would it need to hold profit flat?

- Current profit: revenue $100M minus variable $24M minus fixed $50M = $26M

- New contribution margin: $40K - $12K = $28K per customer

- Customers needed for the same $26M profit: ($26M + $50M) / $28K = $76M / $28K = 2,714 customers

- Required growth: 2,714 minus 2,000 = 714 more customers, a 36% increase

Sanity check: If the total addressable market is 5,000 accounts, the client needs 54% penetration, a stretch. If TAM is 15,000, the 18% penetration is feasible. The decisive question is price elasticity: does a 20% price cut realistically generate 36% more demand? If not, the cut destroys profit. This is why the break-even number is a setup for judgment, not the answer itself.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

How Do You Find the Break-Even Price?

Sometimes the interviewer fixes the volume and asks what price clears costs. Rearrange the same equation to solve for price instead of quantity:

Break-even price = Variable Cost per unit + (Fixed Costs / Expected Volume)

Worked Example 3: A subscription box has $1,200,000 in fixed costs and $18 variable cost per box, and expects to ship 60,000 boxes a year. The lowest price that avoids a loss is:

- Fixed cost per box at this volume = $1,200,000 / 60,000 = $20

- Break-even price = $18 + $20 = $38 per box

Any price above $38 produces profit at 60,000 boxes; any price below it produces a loss unless volume rises. Notice the break-even price falls as expected volume rises, because the fixed cost is spread over more units. That relationship is the single most useful thing to say out loud in a pricing case.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

How Do You Handle a Profit Target Instead of Zero Profit?

Break-even means profit equals zero, but clients rarely want to merely survive. To hit a required return, add the target profit to fixed costs before dividing:

Required Volume = (Fixed Costs + Target Profit) / Contribution Margin

Worked Example 4: Using the earbuds case (fixed costs $2M, contribution margin $24), suppose leadership wants $1.2M of annual profit, not just break-even:

- Required volume = ($2,000,000 + $1,200,000) / $24 = $3,200,000 / $24 = 133,334 units

So break-even is approximately 83,000 units, but the real go/no-go bar is approximately 133,000 units. Confusing the two is a classic stumble: candidates declare victory at break-even when the client's actual hurdle is the profit target.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

What Is Margin of Safety and Why Mention It?

Margin of safety is the cushion between current (or forecast) sales and the break-even point. It tells the client how much demand can fall before the venture starts losing money:

Margin of Safety = (Actual Units - Break-Even Units) / Actual Units

Worked Example 5: If the earbuds line is forecast to sell 100,000 units against a break-even of 83,334:

- Margin of safety = (100,000 - 83,334) / 100,000 = 16,666 / 100,000 = ~17%

Sales can drop 17% before the product turns unprofitable. A thin margin of safety (single digits) signals a fragile launch and is a strong cue to recommend de-risking, such as lowering fixed costs or improving contribution margin, before committing.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

Multi-Product Break-Even

When a company sells multiple products at different margins, compute a weighted-average contribution margin based on the sales mix, then apply the standard formula:

- Product A: $120 price, $70 variable cost, $50 margin, 60% of unit sales

- Product B: $80 price, $50 variable cost, $30 margin, 40% of unit sales

- Weighted contribution margin = ($50 x 0.6) + ($30 x 0.4) = $30 + $12 = $42

- With $840,000 in fixed costs: break-even = $840,000 / $42 = 20,000 total units (12,000 of A and 8,000 of B at the given mix)

State the mix assumption explicitly. If the interviewer shifts the mix toward the higher-margin product, the weighted margin rises and break-even falls, which is itself a strategic lever worth flagging.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

Break-Even vs. Payback Period

Candidates frequently confuse these. The distinction is unit-based versus time-based.

In many cases you need both: first prove the business model can clear its costs (break-even), then judge whether the time to recover the upfront investment is acceptable (payback). For the investment-return side, see the ROI and payback period guide.

What Are the Most Common Break-Even Mistakes?

The fastest way to internalize all five is reps under time pressure, ideally inside full cases where the break-even calc is one step among many. You can practice case math drills on Road to Offer and get instant feedback on both speed and the interpretation step that most candidates skip.

Related Guides

- Profitability framework: break-even tests business viability inside profitability cases, and the calc usually lives in the cost branch of the profit tree.

- Market entry framework: compare your break-even volume against the addressable market to judge whether entry is viable.

- Pricing strategy cases: model how a price change moves contribution margin and the break-even point.

- Consulting math formulas: break-even is one of the core formulas you should be able to recall instantly.

- Mental math for case interviews: practice dividing large numbers fast so the break-even step costs you no time.

- Case interview math practice: drill break-even alongside market sizing and growth math.

- ROI and payback period: the time-based complement to break-even for investment decisions.

- Cost reduction case interview: break-even math sizes how large a cost cut must be to restore viability.

- Restructuring case interview: cash break-even and operational break-even are the two survival metrics in a distressed-company case.

- Case interview cheat sheet: the one-page formula and framework reference, with break-even in the quant section.

Sources

- PrepLounge: Break-Even Analysis in Your Case Interview (checked June 18, 2026)

- CaseBasix: Breakeven Analysis Guide for Case Interviews (checked June 18, 2026)

- Hacking the Case Interview: Break-Even Analysis, Formula & Examples (checked June 18, 2026)

- Management Consulted: Break-Even Analysis (checked June 18, 2026)

- Yale School of Management: A Primer on Breakeven Analysis (checked June 18, 2026)

Frequently asked questions

Resources and related guides

- Learn case math methodPractice

- Browse all free resourcesResource hub

- Case Interview Formulas: Cheat Sheet for Profitability and Math (2026)Math And Quant · May 1, 2026

- Case Interview Math Practice: 30 Drills, Questions, and SolutionsMath And Quant · Feb 6, 2026

- Best Free AI for Case Interview Math Practice (2026)Math And Quant · May 8, 2026

- ROI, NPV & Payback Period for Case Interviews (2026)Math And Quant · Mar 20, 2026