ROI, NPV & Payback Period for Case Interviews (2026)

When to use ROI, NPV, and payback period in case interviews, with formulas, worked examples, and how interviewers score the math.

On this page

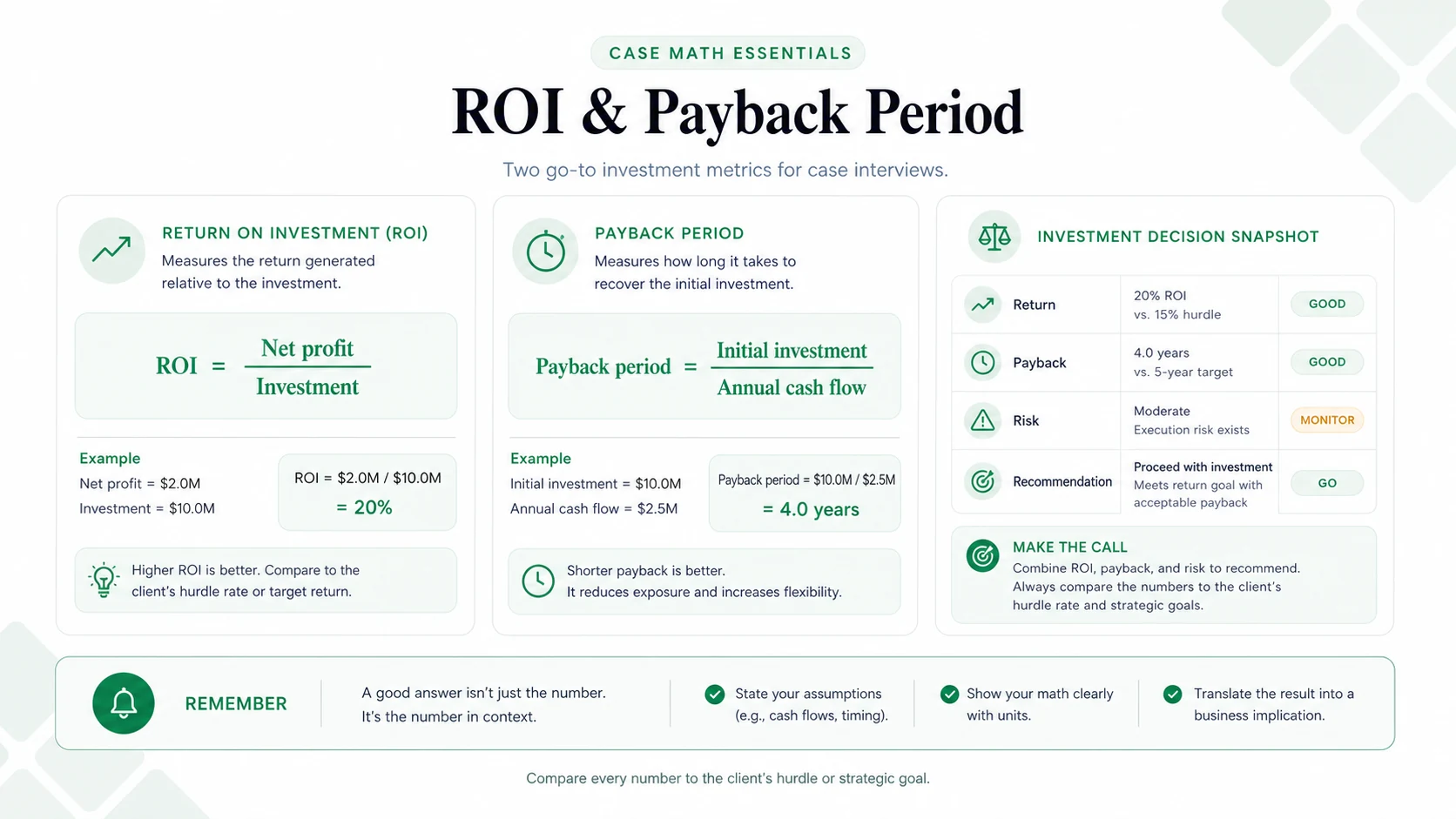

ROI, NPV, and payback period are the three investment-analysis metrics case interviews in 2026 expect you to choose between, not just calculate. ROI measures percentage return (Net Profit / Investment Cost x 100), NPV discounts future cash flows to today's dollars using a discount rate, and payback period calculates the years needed to recover the initial investment. Each has a different blind spot: ROI ignores how long the return took to arrive, payback ignores everything that happens after the money is recovered, and only NPV accounts for the time value of money across uneven, multi-year cash flows. The practical rule, per Corporate Finance Institute's guidance on IRR and discounted cash flow analysis, is to use ROI for quick same-timeline comparisons, switch to NPV once cash flows span 5+ years or vary by period, and lead with payback when the client's real constraint is speed of capital recovery rather than total value created. If the interviewer mentions a discount rate or cost of capital, treat that as an explicit signal to run NPV rather than defaulting to the simpler formulas. This guide walks through all three formulas, a fully worked technology-platform decision, and the mental-math shortcuts that let you calculate NPV in seconds under time pressure.

Need to sharpen your case math?

Road to Offer drills you on ROI, NPV, and payback calculations with timed problems and instant feedback. Build speed without sacrificing accuracy.

The Four Formulas: When to Use Each

ROI is the fastest to calculate and works for comparing investments with similar time horizons. Its limitation: ignoring the time value of money makes 50% ROI over 2 years look identical to 50% over 10 years.

NPV is the most theoretically correct metric, accounting for when cash flows arrive. Use the perpetuity shortcut (Annual Cash Flow / Discount Rate) for constant streams or the annuity factor for equal payments over a fixed period.

- ROI: (Net Profit / Investment Cost) x 100, for quick screening and same-timeline comparisons

- NPV: Sum of [CF_t / (1+r)^t] - Investment, for uneven cash flows, 5+ year horizons, and M&A valuations

- Payback: Investment / Annual Cash Flow, for capital-constrained clients and risk-averse scenarios

- IRR: Rate where NPV = 0, for PE cases with hurdle rates (typically target 20-25%)

Decision Matrix: Which Metric for Which Scenario

If the interviewer does not specify which metric to use, start with payback period (fastest to calculate), add ROI for the return perspective, then offer NPV if the time horizon is long or cash flows are uneven. This shows versatility without overcomplicating the problem.

When the interviewer provides a discount rate or mentions cost of capital, that is an explicit signal to use NPV. PE and M&A contexts with hurdle rates call for IRR.

Use the matrix on a fresh investment prompt before reading the worked example. Choose the metric, show the calculation, and explain what the result changes in the client decision.

Choose and calculate the right investment metric from the Road to Offer drill engine: a real prompt, your answer, and AI-scored feedback. Free account includes free daily drills.

Worked Example: Technology Platform Decision

Prompt: A B2B software company must choose between two investments. Option A: upgrade existing platform for $8M, earning $3M/year for 5 years. Option B: build a new AI platform for $20M, earning $2M (Y1), $4M (Y2), $7M (Y3), $10M (Y4), $12M (Y5). Cost of capital: 12%. Negligible incremental costs.

Option A: Payback = $8M / $3M = 2.67 years. ROI = ($15M - $8M) / $8M = 87.5%. NPV = ($3M x 3.60 annuity factor) - $8M = +$2.8M.

Option B: Payback = 3.7 years (cumulative at Y3: $13M; remaining $7M / $10M Y4 = 0.7 years). ROI = ($35M - $20M) / $20M = 75%. NPV at 12%:

Synthesis: "If capital-constrained or risk-averse, Option A: faster payback (2.7 vs. 3.7 years), higher ROI (87.5% vs. 75%), lower upfront cost ($8M vs. $20M). If the client can absorb higher investment and trusts the Y4-5 projections, Option B creates $400K more value. I would stress-test Option B's NPV by reducing Y4-5 projections 20%."

Mental Math Shortcuts

Speed separates strong candidates from average ones. Memorizing a few key values lets you calculate NPV in 15 seconds instead of building a full table. The Rule of 72 (72 / rate = years to double) provides quick IRR sanity checks: at 10% growth, an investment doubles in ~7.2 years.

For equal annual cash flows, use annuity factors instead of discounting each year individually. For perpetuities, NPV = Cash Flow / Discount Rate. Example: $5M/year at 10% = $50M NPV; if it costs $40M, the investment creates $10M in value.

Annuity factors (memorize these):

Quick discount factors at 10% (approximate):

Now calculate this: put the perpetuity shortcut and the annuity factors above to work on three fresh ROI, NPV, and payback prompts.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

Common Mistakes in Investment Cases

Five errors that cost candidates points in investment analysis cases. Each is avoidable with awareness.

- Confusing revenue with cash flow: Use net cash flow (revenue minus all costs), not gross revenue

- Forgetting initial investment in NPV: Include the outflow at t=0 as a negative; omitting it turns a negative-NPV project positive

- Using ROI across different timeframes: 40% ROI over 2 years (20% annualized) differs vastly from 40% over 8 years (5%); annualize or switch to NPV

- Ignoring opportunity cost: Flag that $20M in Project A means $20M unavailable for alternatives

- Over-precision: Round to nearest $100K or $1M; interviewers test approach, not decimal arithmetic

Master case interview math, not just formulas

Road to Offer tests your ability to choose the right metric, calculate under time pressure, and interpret results in business context. Timed drills with scoring.

Related Guides

- Break-Even Analysis Case Interview: the companion metric to payback period; use both together to frame any investment recommendation

- Consulting Math Formulas: the complete formula reference sheet

- PE Due Diligence Framework: investment analysis in private equity contexts

- Cost Reduction Case Interview: ROI applies directly when the case asks which cost reduction initiative to fund first given capital constraints

- Scale vs. Profitability Case Interview: payback period is the primary financial test for whether to invest in scaling versus protecting current margin

- Profitability Framework: where ROI analysis feeds into profitability recommendations

Sources (checked June 17, 2026)

- Hacking the Case Interview, 26 case interview formulas: hackingthecaseinterview.com/pages/case-interview-formulas

- IGotAnOffer, case interview math guide: igotanoffer.com/blogs/mckinsey-case-interview-blog/case-interview-maths

- Management Consulted, case interview formulas: managementconsulted.com/case-interview-formulas

- Corporate Finance Institute, internal rate of return: corporatefinanceinstitute.com/resources/valuation/internal-rate-return-irr

- Nucleus Research, ROI, TCO, NPV and payback guide: nucleusresearch.com/everything-to-know-about-roi-tco-npv-and-payback

- Wall Street Prep, IRR formula and calculator: wallstreetprep.com/knowledge/irr-internal-rate-of-return

Frequently asked questions

Resources and related guides

- Use it inside a full casePractice

- Browse all free resourcesResource hub

- Best Free AI for Case Interview Math Practice (2026)Math And Quant · May 8, 2026

- Break-Even Analysis for Case Interviews: Formula, Worked Examples, and When to Use It (2026)Math And Quant · Mar 20, 2026

- Consulting Math Formulas: The Case Interview Reference (With Worked Examples)Math And Quant · Mar 15, 2026