Banking Case Interview: Framework, Examples & Prep

Banking case interview guide: inverted balance sheet, net interest margin, four case types, profitability tree, and worked examples.

On this page

The banking case interview in 2026 is one of the few case types where a strong generalist can still freeze, because the business model is genuinely inverted and easy to misread if you treat a bank like a normal company. MyConsultingOffer puts the trap plainly: general frameworks work everywhere, but "some industries have specific issues that make it a lot easier to pass if you know what to expect." Banking is exactly that industry. A retail-bank profit case looks like a normal profitability case until you remember that the loans the bank issues are assets, the deposits it holds are liabilities, and profit comes from the interest spread, not from selling more units. This guide teaches the banking-specific economics first, gives you one reusable profitability tree, and then walks three distinct worked examples (a profit decline, a market-entry, and a pricing or incentive decision) with clean math you can follow line by line. By the end you will recognize the case type on contact and structure from first principles.

What a banking case interview is, and which firms test it

A banking case interview is a consulting case set inside a bank or a financial-services business. Instead of "should this coffee chain expand," you get "our retail bank's profit fell, why," or "should this bank launch a wealth-management arm." The skills are the same (structure, math, judgment, synthesis), but the content assumes you know how a bank makes money.

Three groups of employers test it. First, the MBB financial-services practices: McKinsey, BCG, and Bain all staff large banking teams and ask sector cases in interviews. Second, the specialists and Big Four: Oliver Wyman is the most banking-heavy strategy firm, Strategy& and Deloitte run financial-services cases inside their advisory tracks. Third, banks themselves use case-based interviews. Capital One is the canonical example, where analyst and strategy roles are built around structured business cases rather than pure behavioral chats. If you are recruiting across the whole sector, read the broader financial services case interview guide alongside this one, since insurance and asset-management cases follow different economics again.

Why banking cases break the normal case template

The reason banking cases feel slippery is that the balance sheet is inverted relative to every other business you have studied.

For a normal company, a loan is a liability and inventory is an asset. For a bank, it is the opposite. The loans the bank issues to customers are its assets (they earn interest and get repaid), and the deposits customers place are its liabilities (the bank owes that money back and often pays interest on it). Cash flows in the direction your intuition does not expect.

That single inversion changes where profit comes from. A retailer earns a margin on each unit sold. A bank earns an interest spread: it pays a low rate on deposits and other funding, lends at a higher rate, and pockets the difference. Scale that spread across the whole loan book and you get net interest income (NII), the largest profit engine in most retail and commercial banks. The efficiency of that engine is net interest margin (NIM), the spread expressed against interest-earning assets.

Three more forces shape every banking case:

- Credit risk and loan losses. Some borrowers default. A bank books a loss provision against expected defaults, and that cost sits directly between revenue and profit. A growth plan that ignores credit quality is a trap.

- Capital requirements. Regulators force banks to hold a buffer of capital against their assets. Capital is the bank's shock absorber, and holding it has a cost, so "just lend more" is never free.

- Regulation. Compliance and capital rules constrain which strategic options are even legal, which is why "cut costs" answers that target compliance spend usually fail.

The four banking case types and how to spot them

"Financial services" and "banking" get blurred together in most prep. Separate them. Within banking there are four recognizable case types, each with different economics.

Retail banking is the case you are most likely to get, because the model is the cleanest illustration of NIM and fee income. Commercial banking cases scale up loan sizes and concentrate credit risk; ConsultingCase101 describes realistic commercial parameters such as small-to-midsized loans of $1,000 to $75,000 and a bank operating 120-plus branches across multiple states. Investment banking cases shift the profit engine almost entirely to fees and commissions rather than interest spread. Digital and challenger-bank cases trade the branch network for technology and customer-acquisition economics; for that flavor, the fintech case interview guide goes deeper on payments, neobanks, and lending unit economics.

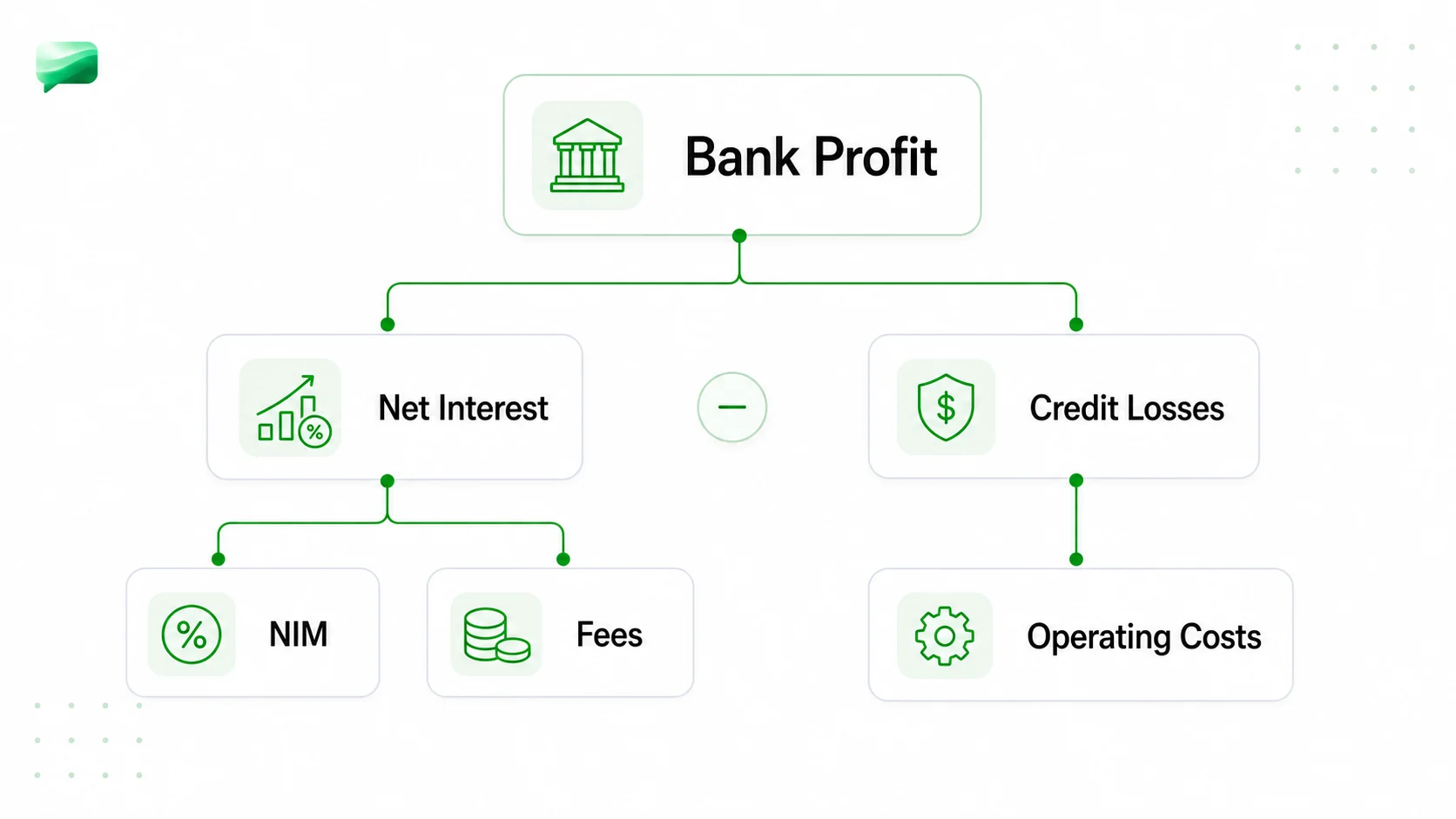

A reusable banking profitability framework

Do not memorize one case. Memorize one tree and adapt it. Layer this banking-specific profit equation on top of the standard four-step case flow (clarify, structure, analyze, recommend). It is the same logic as the general profitability framework, rebuilt around how a bank actually earns.

Bank profit = (Net interest income + Fee / commission income) - Operating cost - Loan losses - Cost of capital

Break each branch down:

- Net interest income = (average loan balance x lending rate) - (average funding balance x funding rate). This is where NIM lives. Diagnose it as rate, volume, or mix.

- Fee / commission income = account fees, payment fees, wealth-management fees, advisory and underwriting commissions. In many cases this is the growth lever when NIM is compressed.

- Operating cost = branches, staff, technology, compliance. Split fixed from variable.

- Loan losses = provisions for expected defaults, driven by credit quality and the economic cycle.

- Cost of capital = the return the bank must earn on the regulatory capital it is forced to hold against its assets.

When you present this, prioritize out loud. In a profit-decline case you walk the whole tree to find the broken branch. In a growth case you focus on the revenue branches and the volume drivers. In a pricing case you zoom into one product's economics. Same tree, different entry point.

Worked example 1: "Our retail bank's profit fell, why?"

Prompt. A large retail bank's annual profit dropped versus a prior year of roughly USD 800 million. Diagnose the cause. (Figures follow the illustrative TheThinksters McKinsey banking example.)

Structure. Walk the profit tree top down. Revenue splits into net interest income (interest income minus interest expense) and commission income. Then subtract operating cost and loan losses.

The diagnostic move. Benchmark the revenue mix against a competitor. In this case, commission income was only about 23% of the bank's total net operating income, versus about 40% for the competitor. That gap is the story: the bank is over-reliant on interest income and under-developed on fees.

Followable math. Suppose total net operating income is roughly USD 2.0 billion.

If this bank closed even half the fee-mix gap, fee income would rise toward USD 630 million, an extra USD 170 million of high-margin revenue that largely drops to profit. That alone could reverse most of the decline against an ~USD 800 million profit base.

Recommendation. The profit fall is a revenue-mix problem, not a cost problem. The bank should grow fee and commission income (payments, cards, wealth advisory) toward competitor levels rather than cutting interest-earning assets. Name the risk: fee growth must not cannibalize the deposit relationships that fund the loan book.

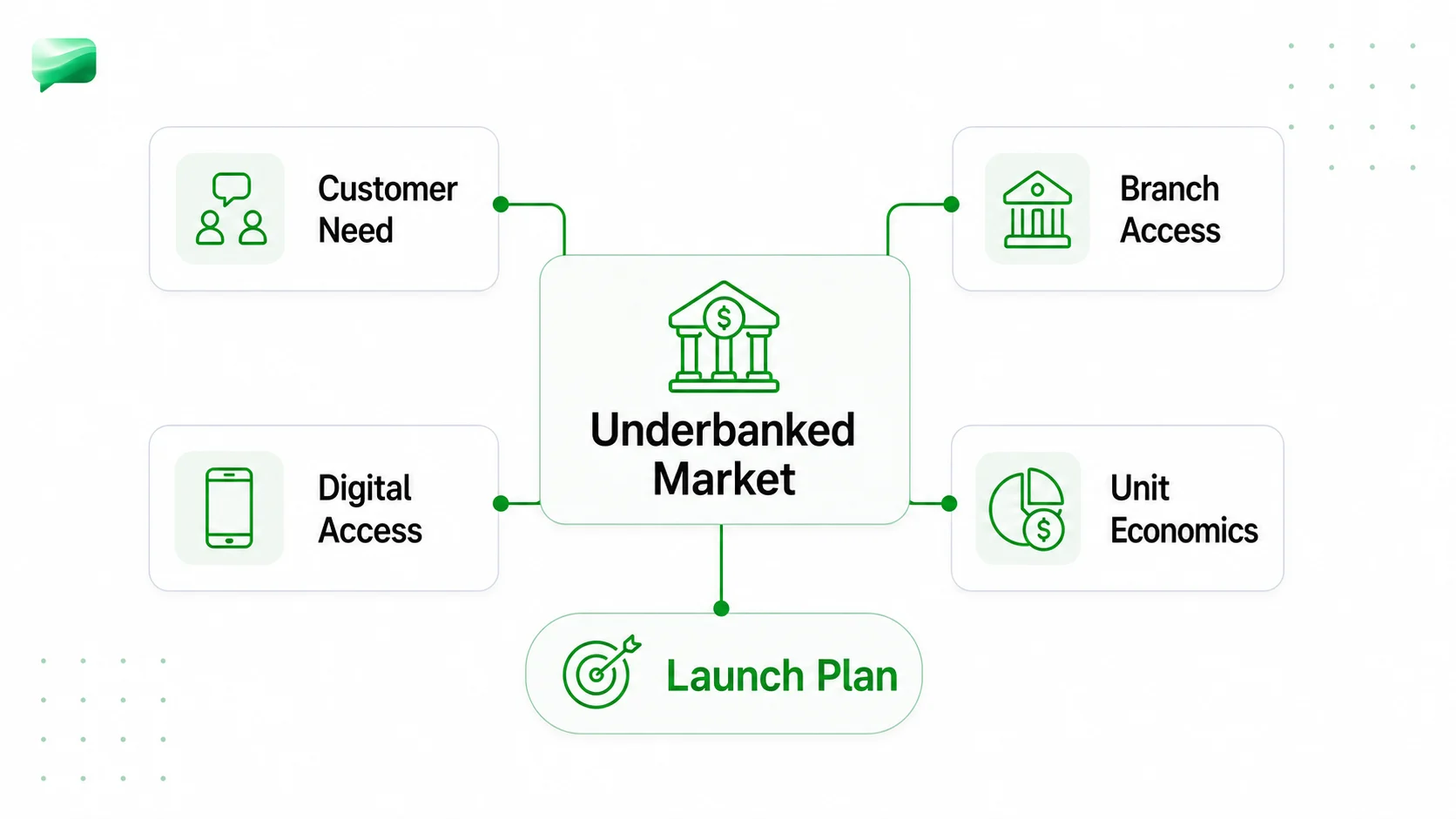

Worked example 2: Growing a retail bank into an underbanked market

Prompt. A bank wants to scale retail operations into an underbanked frontier market. Is it worth entering, and how big could it be? (Figures follow the illustrative MyConsultingOffer financial-services growth case.)

Structure. Growth case, so focus on the revenue branches: market size, customers reachable, products per customer, revenue per product, then net it against cost-to-serve.

Sizing the opportunity. The market has a population over 100 million, but only 10 to 20% currently have access to financial services. That is the entire thesis: 80 to 90% of the population is unbanked and addressable.

Followable math. Take the conservative end.

- Population: 100M. Currently banked at ~15%, so ~85M unbanked.

- Assume the bank can reach 5% of the unbanked in five years: 85M x 5% = 4.25M new customers.

- Assume an agent-based distribution model paying a 0.15% commission per product sold, with the business running at a 5 to 7% profit margin on the revenue it books.

- If each customer generates, say, $40 of annual revenue, that is 4.25M x $40 = $170M revenue, and at a 6% margin, roughly $10M annual profit before scale effects.

Recommendation. Enter, but lead with a low-cost agent or digital distribution model rather than expensive branches, because the unit economics only work at very low cost-to-serve and a tiny commission per product. Flag credit risk and identity/regulatory infrastructure as the gating assumptions to validate before committing capital.

Worked example 3: Should the bank add a commission-based sales incentive?

Prompt. A retail bank is considering paying its salespeople a commission to push products. Is the incentive viable? (This mirrors PrepLounge's Retail Banking Profitability case, which has been solved 15.8k times, a useful signal of how standard this archetype is.)

Structure. Pricing / viability case, so zoom into per-product economics: what the bank earns per product, what the incentive costs per product, and how much extra revenue the incentive must drive to pay for itself.

Followable math. Per the PrepLounge figures:

The logic: paying the salesforce adds about $16 of cost to every product sold. For the incentive to be worth it, the extra sales it generates must cover that cost. The case pegs the break-even at a 6.67% lift in revenue. Below that, the commission destroys value; above it, the incentive pays for itself.

Recommendation. Approve the incentive only if the bank reasonably believes salespeople can lift product revenue by more than ~6.67%, and only on products where the $80 operating profit is real after loan losses. Watch for two traps: product cannibalization (paying commission on sales that would have happened anyway) and pushing unsuitable products to hit targets, which carries regulatory and reputational cost.

The banking math and terminology interviewers expect

Banking jargon is where unprepared candidates stall. Learn this short glossary and the math becomes routine.

You do not need to compute these to four decimals. You need to know which one the case hinges on and reason cleanly in two or three steps. If your arithmetic wobbles under pressure, that is a drill problem, not a knowledge problem.

Banking-specific clarifying questions to open with

Before you structure, confirm the business model. Strong banking candidates open with targeted questions, not generic ones:

- Bank type. Is this a retail, commercial, investment, or digital challenger bank? The profit engine differs by type.

- Product mix. Which products dominate: deposits, mortgages, cards, business loans, wealth, advisory?

- Customer segments. Mass-market retail, affluent, small business, or corporate?

- Geographic footprint. One market or many? How many branches, and is distribution physical or digital?

- Current performance. What is the bank's NIM, fee-income share, and profit today, and how does that compare to last year and to competitors?

These five questions take 60 seconds and immediately frame which branch of the profit tree matters most.

How to pass a banking case

Five habits separate candidates who pass banking cases from those who recite a framework and hope.

- Validate the business model first. Before structuring, confirm how this specific bank makes money. A 20-second model check stops you from solving a retail case with an investment-banking structure.

- Align on the success metric. Profit, ROE, NIM, or customer growth? Pin the metric the interviewer cares about so your analysis and recommendation land on the same target.

- Structure from first principles. Build the profit tree (NII + fee income, minus cost, loan losses, cost of capital) live, rather than forcing a memorized 4-box framework onto a balance-sheet business.

- Stay calm with unfamiliar jargon. If a term is new, ask. "When you say combined funding cost, do you mean deposits plus wholesale borrowing?" reads as confidence, not weakness.

- Quantify, then recommend with a risk. Size the lever in dollars (the fee-mix gap, the break-even lift), lead with the answer, and name the one risk that could break it.

Practice these on real cases, not just by reading. Run a banking-flavored profitability case, then a growth case, and review your structure and math against the model each time.

Sources

- PrepLounge, Retail Banking Profitability case (checked June 26, 2026)

- TheThinksters, McKinsey banking-sector case example (checked June 26, 2026)

- MyConsultingOffer, financial services case interview (checked June 26, 2026)

- ConsultingCase101, banking cases tag (checked June 26, 2026)

FAQ

Frequently asked questions

Keep reading

- Insurance Case Interview: Framework, Ratios & ExampleFundamentals · Jun 30, 2026

- Automotive Case Interview: Value Chain, Examples & PrepFundamentals · Jun 30, 2026

- Consumer Goods Case Interview: CPG Frameworks & ExamplesFundamentals · Jun 30, 2026

- Operations Case Interview: Framework, Math & ExampleFundamentals · Jun 30, 2026