Private Equity Case Interview: LBO, Screening, and CDD

A practical guide to private equity case interviews, including deal screening, paper LBO math, commercial due diligence, and a worked example.

On this page

A private equity case interview in 2026 asks a tighter question than a typical consulting case: should we buy this business, at what price, and what would make the deal work? Where a consulting case tests open-ended strategy, a PE case tests a simple deal-screening framework, back-of-the-envelope LBO math, and commercial due diligence that explains whether the target's revenue is actually defensible after the deal closes. According to eFinancialCareers, candidates from a consulting background tend to be too focused on the qualitative elements, while candidates from banking tend to be too focused on getting the numbers right, and the case is built to catch exactly that gap. A strong answer holds both halves together: the qualitative investment thesis covering market, moat, and management, plus the quantitative return math covering entry multiple, leverage, exit multiple, and IRR, then lands on one clear buy, pass, or diligence-further call, with the specific risks and the data you would still verify before committing capital.

PE Cases vs. Consulting Cases: The Core Difference

Most candidates from consulting backgrounds spend 80% of their time on qualitative analysis and forget to anchor in a return target. Banking candidates make the opposite error: they get lost in numbers and cannot articulate why the business is worth buying. According to eFinancialCareers, "consultants are often too focused on the qualitative elements and bankers are too focused on getting the numbers right."

The deepest conceptual difference: a great company at 20x EBITDA might be a terrible investment. A mediocre business at 5x EBITDA might be a home run if you can cut costs and exit at 8x. PE interviews test whether you can hold both ideas simultaneously.

A Simple Deal Screening Framework

Structure every PE case (live or take-home CIM) across four layers that map directly to what a real investment team evaluates before an IC presentation.

Layer 1: Market Assessment. Is this a market worth underwriting? You care about size, growth, and whether the demand story is durable enough to support a future exit.

Layer 2: Competitive Position. What is the moat? Switching costs, network effects, regulatory barriers, cost advantages, or brand pricing power. In an interview, support each claim with evidence such as churn, margin advantage versus peers, or pricing premium. A company with no identifiable moat means you may be dependent heavily on financial engineering for returns.

Layer 3: Financial Profile. Pull revenue growth, EBITDA margin and trend direction, free cash flow conversion, working capital behavior, and leverage capacity.

Layer 4: Exit Strategy. Who buys this in 5-7 years? Strategic acquirer (1-2x additional multiple turns), secondary PE (if growth runway remains), or IPO (viable only for $500M+ revenue, high-growth businesses). The exit is how LPs get paid, so you need a credible path before committing capital.

LBO Basics: The Math You Must Know

An LBO acquires a company using debt plus equity, improves the business over time, pays down debt with free cash flow, and then exits at a later valuation. Wall Street Prep is still the cleanest simple reference for the mechanics.

Paper LBO: the mental math format. Many first-round interviews use a paper LBO: a 5-30 minute pen-and-paper calculation. Memorize the MOIC-to-IRR conversion table:

Many interviewers use ~20% IRR as a shorthand hurdle in paper LBO cases, but the exact target varies by fund, strategy, and market conditions. For mental math fluency, see our guide to mental math shortcuts for case interviews.

Commercial Due Diligence: The 5 Questions

Consulting firms are frequently hired by PE funds to conduct CDD on acquisition targets. CDD answers the fundamental question: is the business model defensible after acquisition?

1. Market size and growth: How large is the addressable market, and what is the 5-year growth CAGR? Is growth driven by secular trend, pricing, or volume?

2. Competitive position: What market share does the target hold? Is share growing, flat, or eroding? What would it take to lose a major account?

3. Customer quality: How concentrated is the customer base? Healthy businesses usually show diversified revenue, durable contracts, and low churn. A single large customer with no long-term contract is a classic diligence risk.

4. Pricing power: Has the company raised prices above inflation in the last 3 years? Is pricing cost-plus or value-based?

5. Management and scalability: Does the company depend on 1-2 key people? Can revenue scale without proportional cost increases?

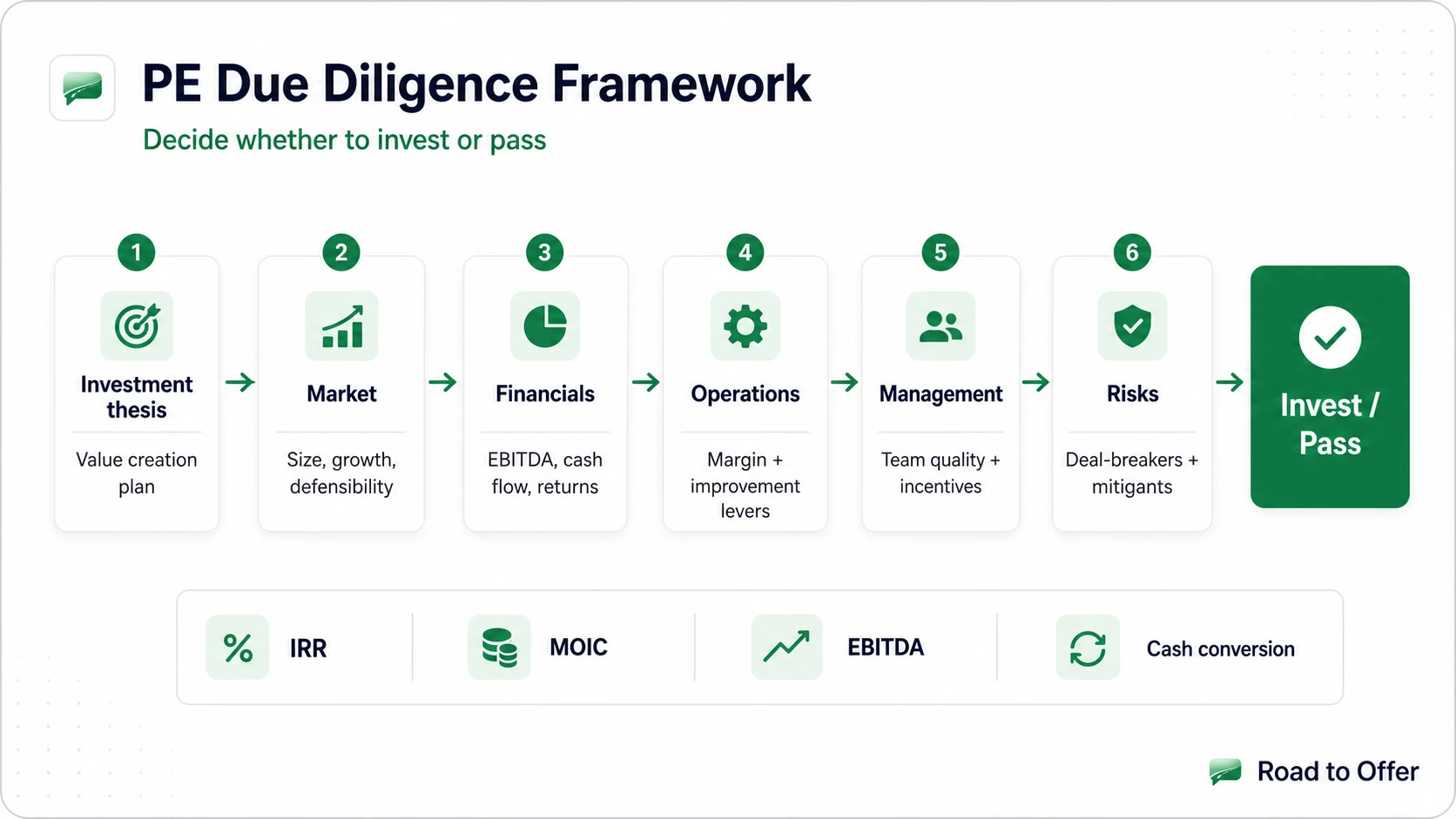

For deeper diligence structuring, see our PE due diligence framework.

For consulting firms that test this same commercial due diligence logic, use the EY-Parthenon case interview guide and L.E.K. case interview guide as firm-specific companions.

Worked Example: Full PE Case Walkthrough

Prompt: Your PE firm is evaluating MedTrack, a software company providing scheduling and compliance tools to outpatient physical therapy clinics. Financials: $40M revenue, $12M EBITDA (30% margin), growing 12% annually. Asking price: $96M (8x EBITDA).

Market assessment: The market is specialized but still large enough to matter, and the target appears to hold meaningful share in a fragmented space. Healthcare workflow software, like the financial software you would evaluate in a fintech case interview, also tends to be stickier than discretionary software categories.

Competitive position: B2B SaaS for healthcare has high switching costs; migrating scheduling and compliance data is painful. NPS is 72 (industry average: 45). Customer churn: 4%. Top 10 customers represent 22% of revenue.

Financial profile and entry structure: Purchase price $96M. Debt at 5x EBITDA = $60M. Entry equity: $36M. FCF conversion approximately 75% = $9M/year.

Exit analysis (5-year hold): EBITDA at year 5 at 12% growth: approximately $21M. Exit multiple: 10x. Exit EV: $210M. Debt paydown: $9M x 5 = $45M repaid, remaining debt $15M. Exit equity: $195M. MOIC: 5.4x. The return clears a typical interview hurdle comfortably.

Interactive drill set. Write an answer before revealing the worked solution, then continue into Road to Offer for scored practice and AI feedback.

Sensitivity: Even at a more conservative exit, the deal still looks investable. That is the real point of the sensitivity check: can the deal survive a less generous market?

Recommendation: Strong invest. Key risk is customer concentration in larger clinic chains; mitigation is negotiating multi-year contracts as a closing condition.

M&A · medium

Practice a buy-side acquisition case with deal math

Healthcare / Digital Health

Common Mistakes in PE Case Interviews

Not anchoring in return math. Every qualitative statement must connect back to value creation: "strong brand loyalty" leads to "pricing power" leads to "sustained 30% EBITDA margins at exit" leads to "confidence in 8-9x exit multiple." Mergers & Inquisitions emphasizes that PE interviews test investment judgment: distinguishing a great company from a great investment.

Ignoring the downside case. If your deal only works because multiples expand from 7x to 10x, it is a weak thesis. A robust deal generates 2.0-2.5x MOIC on debt paydown and EBITDA growth alone, with multiple expansion as upside.

Treating CDD like a consulting case. CDD in a PE context is not open-ended strategy. It answers one question: is revenue defensible post-acquisition? Stay focused on moat durability, customer retention, and pricing power, not on blue-sky growth opportunities.

Missing customer concentration risk. Peak Frameworks notes that top 3 customers representing 50%+ of revenue is existential risk. Always quantify the downside scenario of losing the largest customer and model the IRR impact.

Related Guides

- PE Due Diligence Framework: operational and financial diligence in depth

- M&A Case Framework: synergy analysis and deal structure questions

- Profitability Framework: margin analysis for EBITDA improvement potential

- Market Entry Framework: translates to market assessment in deal screening

- Market Sizing Guide: structured approach for TAM estimation in PE cases

- Case Interview Frameworks Guide: selecting the right framework when type is ambiguous

See where you stand on PE and consulting case skills

Take Road to Offer's free assessment to benchmark your deal screening, LBO logic, and commercial due diligence skills, with a personalized improvement plan.

Sources (checked June 17, 2026)

- Bain, Global Private Equity Report 2025: bain.com/insights/outlook-is-a-recovery-starting-to-take-shape-global-private-equity-report-2025

- Wall Street Prep, LBO model basics: wallstreetprep.com/knowledge/basics-of-an-lbo-model

- Wall Street Prep, Paper LBO guide: wallstreetprep.com/knowledge/paper-lbo

- Corporate Finance Institute, Paper LBO tutorial: corporatefinanceinstitute.com/resources/career/paper-lbo

- Mergers & Inquisitions, PE interviews: mergersandinquisitions.com/private-equity-interviews

- eFinancialCareers, PE case study interview: efinancialcareers.com/news/private-equity-case-study-interview

- Baker Tilly, Market diligence for PE: bakertilly.com/insights/three-aspects-of-market-diligence-private-equity-firms

Frequently asked questions

Resources and related guides

- Start Quick MathPractice

- Browse all free resourcesResource hub

- 3Cs Framework: Company, Customer, Competitor (Worked Example)Frameworks · Feb 6, 2026

- 4C Framework Case Interview: The 4 Cs, a Worked Example & How to Use It (2026)Frameworks · Jun 28, 2026

- 4Ps Framework Case Interview: Product, Price, Place, PromotionFrameworks · Feb 6, 2026