PE Due Diligence Framework for Case Interviews (2026)

PE due diligence framework for case interviews: market assessment, financial analysis, operational improvement, and a worked acquisition example.

On this page

A PE due diligence framework is a structured approach for evaluating whether a private equity fund should acquire a target company, covering market assessment, financial analysis (EBITDA, IRR, MOIC), operational improvement potential, management quality, and risk. These cases appear in 25-30% of Bain interviews and 10-15% of cases at McKinsey, BCG, and Deloitte.

The core difference between a PE case and a standard M&A case: PE buyers think in terms of investment returns (IRR, MOIC) and value creation plans, not just strategic fit. Every analysis must connect to "Will this make money for the fund?"

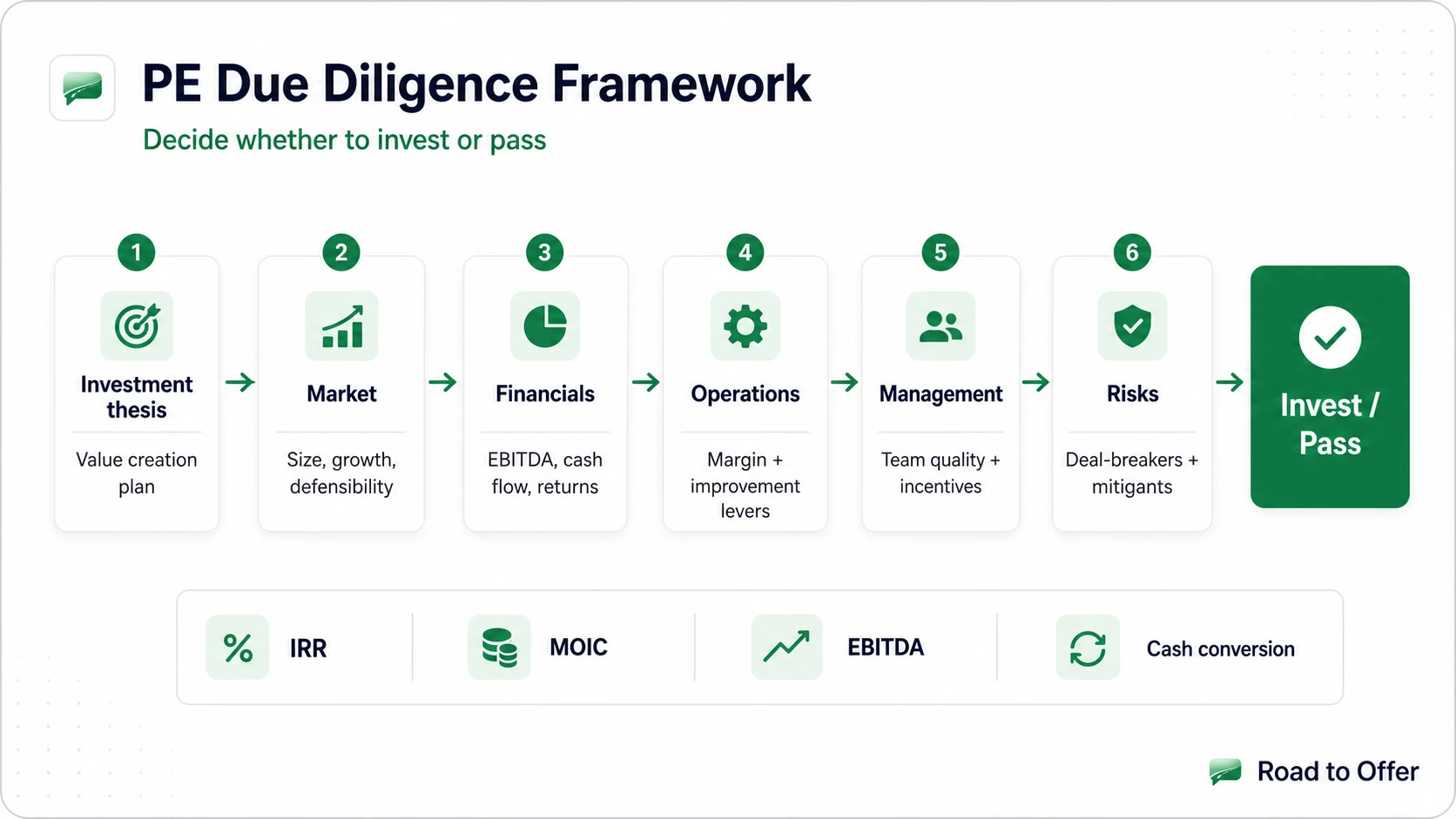

The PE Due Diligence Framework

Step 1: Clarify the Investment Thesis

Before diving into analysis, understand why the PE fund is interested in this target. The investment thesis is the story of how the fund will make money. Common PE investment theses include:

- Operational improvement: The target is underperforming operationally and the fund can improve margins through cost reduction, procurement optimization, or process efficiency.

- Revenue growth: The target has untapped growth potential (new markets, new products, pricing power) that the fund can unlock.

- Platform / roll-up: The target is a platform for acquiring smaller companies in a fragmented industry, building scale and market share.

- Financial engineering: The target generates stable cash flows that support leverage, and the fund can create returns primarily through debt paydown.

- Market timing: The industry is undervalued or at an inflection point, and the fund believes it can buy low and sell high.

Step 2: Market Assessment

Evaluate the market where the target operates. PE funds want markets that are:

Market size and growth:

- How large is the addressable market?

- What's the historical growth rate (CAGR over 5-10 years)?

- What's the projected growth rate?

- What's driving growth (or decline)?

Market structure:

- How fragmented or concentrated is the market?

- What's the competitive landscape? Who are the top 3-5 players and what's their market share?

- Are there barriers to entry (regulation, capital requirements, brand, distribution)?

- Is there pricing power or is the market commoditized?

Market resilience:

- How cyclical is the market?

- How recession-resistant are revenues?

- Are there regulatory or technological disruption risks?

A PE fund typically targets markets that are growing at or above GDP, have moderate fragmentation (consolidation opportunity), and demonstrate recession resilience (predictable cash flows support leverage).

Step 3: Financial Analysis

The financial deep-dive is the quantitative core of PE due diligence. Key metrics:

Revenue Analysis

- Revenue trend: Is revenue growing, flat, or declining? What's the CAGR?

- Revenue quality: Is growth organic or acquisition-driven? Recurring vs one-time?

- Revenue concentration: What percentage comes from the top 5-10 customers? High concentration is a risk.

- Pricing dynamics: Can the target raise prices? What's the historical price vs volume split?

Profitability Analysis

- EBITDA and EBITDA margin: The primary profitability metric in PE. How does it compare to peers?

- Margin trend: Are margins expanding, stable, or compressing? Why?

- Cost structure: Fixed vs variable cost breakdown. What's the operating leverage?

- Unit economics: What's the per-unit or per-customer profitability?

Cash Flow Analysis

- Free cash flow (FCF): EBITDA minus capex minus working capital changes. This is what services the debt.

- Cash conversion: FCF / EBITDA. Above 70% is healthy; below 50% raises questions.

- Working capital dynamics: Is working capital increasing faster than revenue? This consumes cash.

- Capex requirements: Maintenance capex vs growth capex. High maintenance capex reduces cash available for debt service.

Return Metrics

- Entry multiple: Purchase price / EBITDA. The lower the entry multiple, the better the returns (all else equal).

- IRR (Internal Rate of Return): The annualized return on equity. PE funds typically target 20-25%+ IRR.

- MOIC (Multiple on Invested Capital): Total return / equity invested. A 2.0x MOIC means the fund doubled its money.

- Exit multiple: Expected sale price / EBITDA at exit. Usually assumes the same or slightly higher multiple than entry.

Step 4: Operational Improvement Assessment

This is where PE consulting work is most concentrated. Identify specific value creation levers:

Revenue Enhancement

- Pricing optimization: Can the target raise prices? What's the price elasticity?

- Sales force effectiveness: Can conversion rates, deal sizes, or customer lifetime value be improved?

- Cross-sell / upsell: Are there adjacent products or services to sell to existing customers?

- Geographic expansion: Can the target enter new regions with existing products?

- Channel optimization: Can the target shift to higher-margin channels?

Cost Reduction

- Procurement: Supplier consolidation, competitive bidding, specification redesign.

- Operations: Lean manufacturing, automation, capacity utilization improvement.

- SG&A: Shared services, overhead reduction, management layer optimization.

- Supply chain: Network optimization, inventory management, logistics efficiency.

For a deep dive into cost levers: Operations & Cost Optimization Framework

Capital Efficiency

- Working capital: Improve receivables collection, extend payables, optimize inventory turns.

- Capex: Reduce capex intensity through asset-light strategies or technology substitution.

- Asset monetization: Sell non-core assets or real estate.

Step 5: Management Team Evaluation

PE funds invest in management teams as much as businesses. Evaluate:

- Track record: Has the team grown revenue, improved margins, or successfully executed transformations before?

- Depth: Is the team deep enough to execute the value creation plan, or are there key-person dependencies?

- Alignment: Will management have equity incentives (typically 5-15% of equity) that align their interests with the fund's?

- Gaps: Are there capabilities the team lacks that the fund would need to recruit for? (Common: CFO upgrade for a PE-backed company.)

- Culture: Is the management team comfortable with PE-level performance expectations (aggressive targets, board oversight, regular reporting)?

Step 6: Risk Assessment

Structure risks as either deal-breakers or manageable risks with mitigants:

Worked Example: Regional Veterinary Clinic Chain

Case prompt: A mid-market PE fund is evaluating the acquisition of PetCare Partners, a regional chain of 25 veterinary clinics across the Southeastern US. The asking price is $120M. Should the fund proceed?

A. Investment Thesis

The fund's thesis is a platform roll-up: acquire PetCare as a platform, then add 15-20 smaller clinics over 3-4 years to build scale, improve procurement leverage, and centralize back-office operations. The vet services market is highly fragmented (top 5 players have less than 15% combined market share) and growing.

B. Market Assessment

- Market size: US veterinary services market is approximately $35B and growing at 6-7% CAGR, driven by rising pet ownership, "humanization" of pets, and increasing spend per visit.

- Fragmentation: Highly fragmented. 85% of clinics are independently owned. National chains (VCA, NVA, Mars Veterinary) have been consolidating aggressively.

- Barriers: Moderate, veterinarian licensing requirements and local reputation create switching costs, but no major capital or technology barriers.

- Recession resilience: Vet spending is moderately recession-resistant. Wellness visits decline slightly in downturns, but emergency and chronic care are non-discretionary.

C. Financial Analysis

Purchase price: $120M at 10x EBITDA. Equity invested: $48M (assuming 60% leverage, $72M debt). Debt/EBITDA: 6.0x (high, but serviceable given stable cash flows).

D. Value Creation Plan

Revenue growth (Years 1-5):

- Organic same-clinic growth: 5% per year (in line with market)

- Add-on acquisitions: 15-20 clinics at 6-8x EBITDA (smaller clinics trade at lower multiples)

- Projected revenue at exit: $160-180M

EBITDA margin improvement:

- Centralize procurement (medical supplies, pharmaceuticals): +1.5pp

- Shared back-office (billing, scheduling, HR): +1pp

- Revenue per visit optimization (upsell wellness plans): +0.5pp

- Target EBITDA margin at exit: 18-19% (vs 15% today)

Projected exit EBITDA: $29-34M (vs $12M at entry) Projected exit at 10x: $290-340M MOIC: $290-340M / $48M equity = 6.0-7.1x over 5 years Implied IRR: 43-48% (highly attractive)

E. Risk Assessment

- Integration complexity: Managing 40-45 clinics across multiple states is operationally complex. Mitigant: hire an experienced COO with multi-site healthcare management experience.

- Veterinarian retention: Vets are in high demand and may leave after acquisition. Mitigant: equity participation for clinic-level leaders, retention bonuses, and autonomy on clinical decisions.

- Overpaying for add-ons: Competition from other consolidators (NVA, Mars) may drive up acquisition prices. Mitigant: focus on clinics in secondary markets where competition for acquisitions is lower.

- Leverage risk: 6.0x Debt/EBITDA is aggressive. Mitigant: stable cash flows (75% cash conversion) and rapid EBITDA growth from add-ons will delever quickly.

F. Recommendation

"I recommend proceeding with the acquisition. The vet services market is attractive: $35B, growing 6-7% annually, highly fragmented, and recession-resistant. PetCare's margin gap vs best-in-class (15% vs 18-20%) represents a clear operational improvement opportunity worth 3-5pp. The roll-up thesis is compelling: smaller clinics trade at 6-8x vs the platform's 10x, creating immediate value on each add-on. The projected returns are strong: 6-7x MOIC and 43-48% IRR over 5 years. The primary risk is integration execution, which I'd mitigate by hiring an experienced multi-site healthcare operator as COO before closing. I'd negotiate to acquire below 10x if possible, as the current margin profile doesn't yet justify a premium multiple."

M&A · medium

Practice a live acquisition diligence case

Logistics / SaaS

Common Mistakes in PE Cases

- Analyzing like a strategic acquirer, not a financial buyer. PE funds care about returns (IRR, MOIC), not just strategic fit. Every recommendation must connect to "Will this generate the target return?"

- Ignoring the value creation plan. Identifying that the target is a good business is not enough. The fund needs a plan: what will they DO to create value? Cost reduction? Revenue growth? Multiple expansion?

- Not checking the leverage. Debt is central to PE returns. A highly leveraged deal amplifies both gains and losses. Always consider whether the target's cash flows can service the debt, especially in a downside scenario.

- Missing the exit. PE funds don't hold forever. Who will buy this company in 3-5 years? At what multiple? If there's no clear exit path, the deal doesn't work regardless of operational improvements.

- Skipping management. The best business with the wrong management team will underperform. And in PE, the management team is executing under intense performance pressure. Flag key-person risks and capability gaps.

Interactive Drills: PE Due Diligence Practice

Related Frameworks

PE due diligence connects to several other case types:

- Case Interview Frameworks Complete Guide, the master selector that shows how PE due diligence extends the M&A framework with financial return and portfolio value creation analysis

- M&A Case Framework, the strategic M&A framework (PE cases add financial return analysis)

- Profitability Framework, used within PE cases to diagnose margin improvement potential

- Value Chain Framework, for identifying where operational improvements can create value after acquisition

- Operations & Cost Optimization Framework, for building value creation plans

- Growth Strategy Cases, for evaluating revenue growth levers at portfolio companies

- Bain Case Interview Guide, PE cases are most common at Bain

Sources and Further Reading (checked June 17, 2026)

- Bain Capital overview: baincapital.com

- Bain Private Equity practice: bain.com/industry-expertise/private-equity

- McKinsey Private Equity practice: mckinsey.com/industries/private-equity-and-principal-investors

- Bain Global Private Equity Report: bain.com/insights/topics/global-private-equity-report

- PrepLounge PE due diligence guide: preplounge.com/en/case-interview-basics/case-cracking-toolbox/identify-your-case-type/private-equity-case

- CaseInterview.com, PE case overview: caseinterview.com/case-interview-frameworks

FAQ