M&A Case Interview Framework: 5 Steps + Synergy Math (2026)

A practical M&A case interview framework: test strategic fit, quantify synergies, evaluate risks, and make a clear recommendation.

On this page

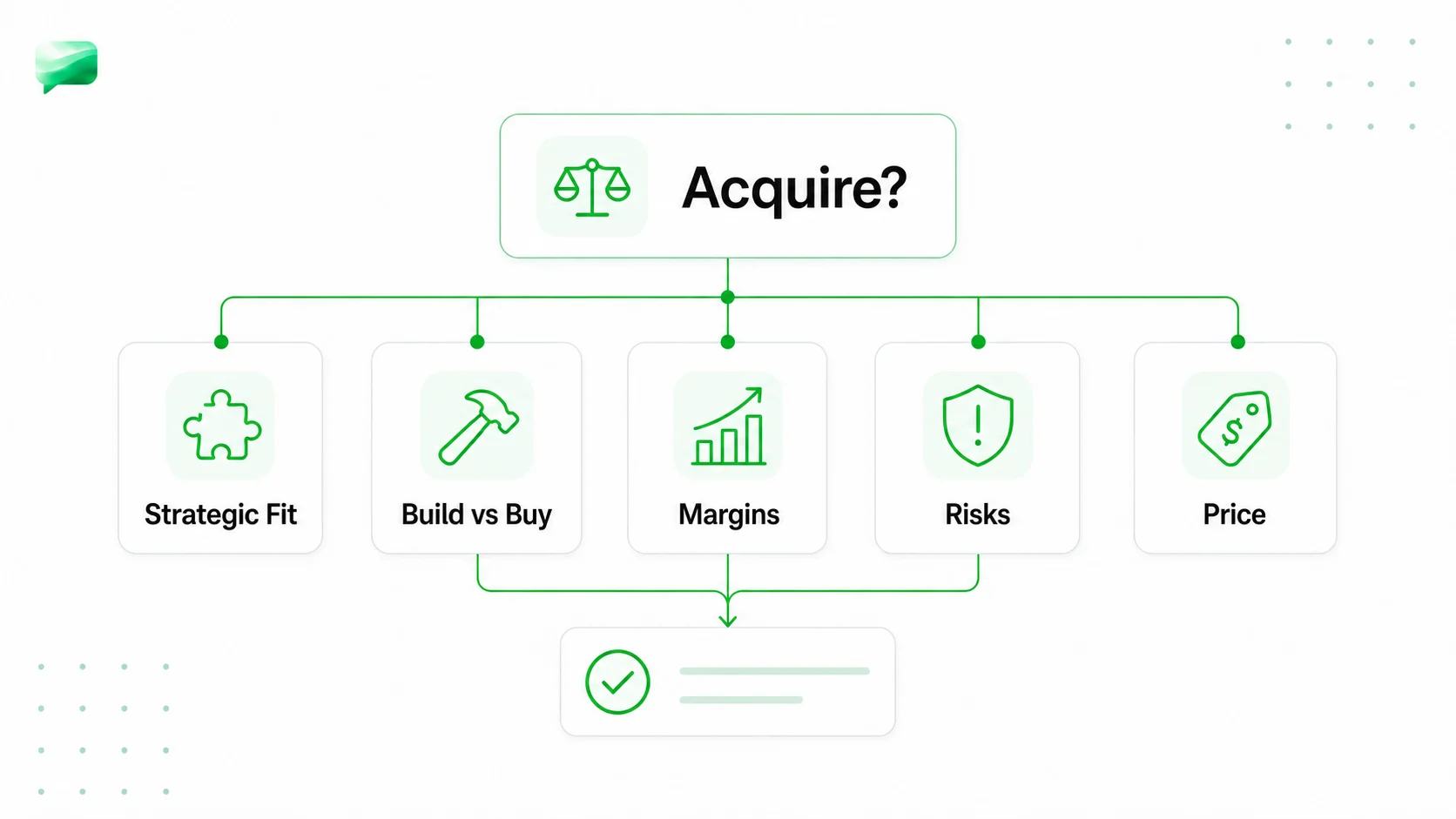

An M&A case interview framework is a structured method for evaluating whether a company should acquire a target by testing strategic fit, quantifying synergies, assessing integration risk, and delivering a go/no-go recommendation with a specific price range. Roughly 70% of acquisitions fail to create the value they promised. M&A cases appear in 15-20% of MBB second-round interviews, making this one of the highest-stakes case types you will face.

According to repeated studies by McKinsey, Bain, and Harvard Business Review, most deals destroy shareholder value. The interviewer is not looking for someone who says "yes, acquire" or "no, don't." They want to see you use an M&A case interview framework that connects strategic logic, financial math, and execution realism into one clear recommendation.

M&A cases show up in roughly 15-20% of second-round interviews at MBB, according to PrepLounge's M&A case overview and Management Consulted's case interview types guide. They are especially common at BCG and Bain, both of which have large private equity and transaction advisory practices, so if BCG is a target, drill timed BCG case interview practice alongside this framework. IGotAnOffer's M&A case guide notes that M&A cases are also growing in frequency at strategy boutiques and Big 4 Transaction Services teams. If you are preparing for those firms, this framework is essential.

What Is an M&A Case Interview Framework?

An M&A (mergers and acquisitions) case asks whether a company should acquire a target and, if so, at what price. In practice, an M&A case interview framework and a merger and acquisition case framework mean the same thing: evaluate strategic rationale, quantify cost and revenue synergies, assess integration risk, and deliver a go/no-go recommendation with financial guardrails. For related frameworks, see growth strategy cases and market entry analysis.

The M&A Case Framework in 5 Steps

This framework works for every M&A case you will encounter in consulting interviews: horizontal acquisitions, vertical integration, PE bolt-ons, and capability buys. The depth you spend on each step will vary by prompt, but the sequence is stable.

A single timed rep tells you fast whether your instinct for the M&A structure holds up before you rely on it in a real interview.

Case Prep Playbook

Learn frameworks properly

Pick and adapt structures instead of memorizing buckets.

Step 1: Strategic Rationale

Before you touch any numbers, answer the core question: why would our client buy this company instead of building the capability internally or partnering?

There are four common strategic rationales for acquisitions:

- Capability acquisition. The target has technology, talent, or IP that would take years to build. Think of a traditional bank acquiring a fintech for its payments platform.

- Market consolidation. Buying a competitor to gain market share, pricing power, or scale economies. Common in fragmented industries like waste management or specialty chemicals.

- Geographic or channel expansion. Acquiring a company to enter a new region or access a distribution network, faster than building from scratch. This overlaps with market entry framework logic.

- Vertical integration. Acquiring a supplier or distributor to capture margin, secure supply, or improve coordination. Think of a retailer acquiring a logistics provider.

Build vs. buy vs. partner test

If the client has time and the capability is not scarce, building is usually cheaper. If speed matters and a good target exists, acquisition makes sense. This is the first judgment the interviewer wants to see.

Step 2: Evaluate Target Attractiveness

Once strategic rationale is established, evaluate whether this specific target is worth acquiring. This is where you apply a profitability framework-style lens to the target's standalone business.

Key dimensions to assess:

Market position and competitive dynamics

- What is the target's market share? Is it growing or declining?

- How does the target compete: on price, differentiation, or niche specialization?

- What is the competitive structure? Use a simplified Porter's Five Forces lens if the interviewer gives you industry data.

Financial health

- Revenue growth trajectory (last 3 years)

- Margin profile: gross margin, EBITDA margin, and trend direction

- Customer concentration: if the top 3 customers represent 50%+ of revenue, that is a risk flag

- Recurring vs. one-time revenue: recurring revenue (subscriptions, long-term contracts) is worth more

Capability and asset quality

- What does the target have that we do not? Technology, talent, patents, distribution, brand?

- How transferable are those assets post-acquisition? A team that leaves after the deal closes is a depreciating asset.

- What is the overlap with our existing business? High overlap means more cost synergy potential but less incremental capability.

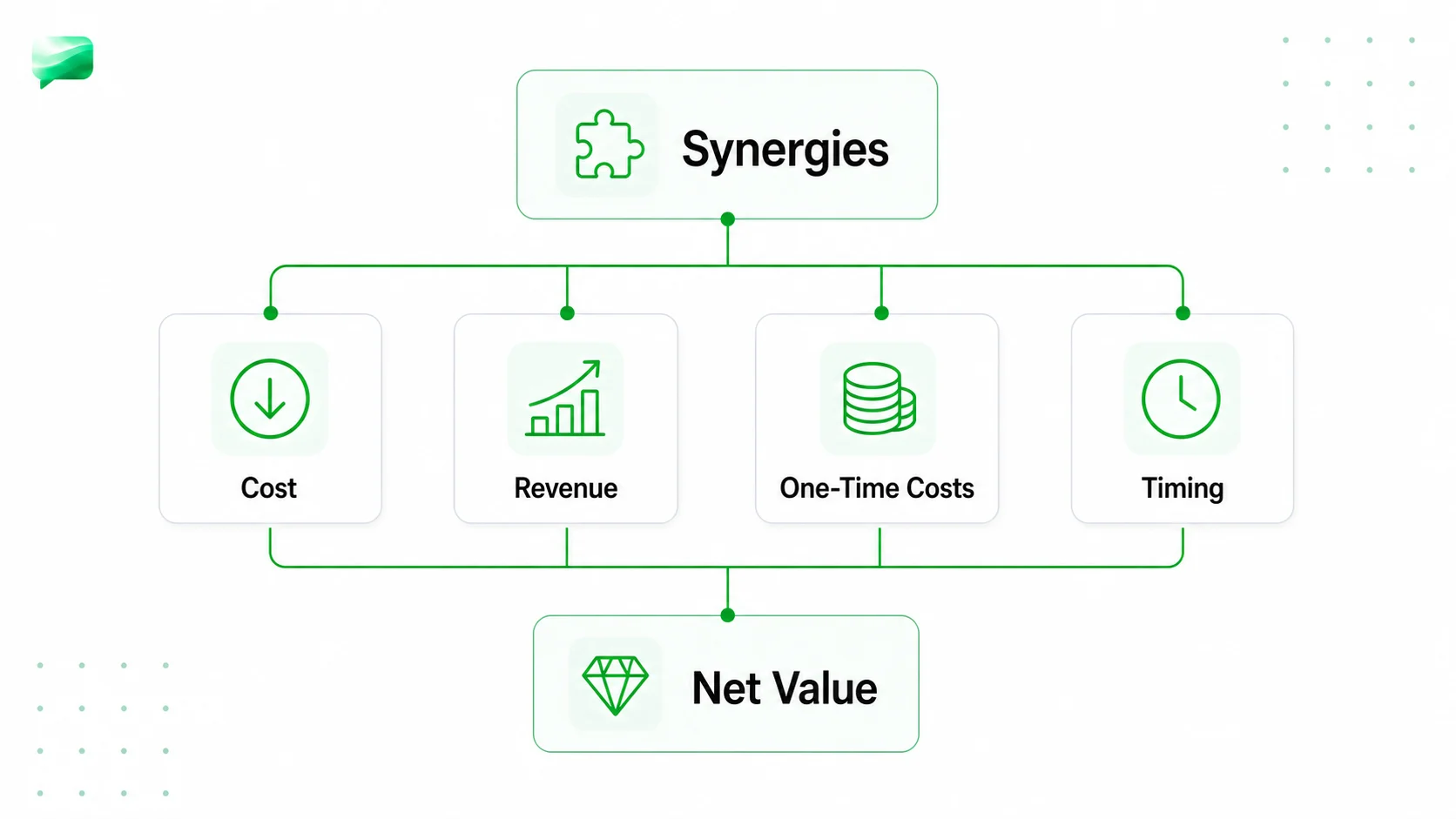

Step 3: Quantify Synergies

This is the math section that makes or breaks your M&A case. Interviewers want to see you break synergies into specific, quantifiable buckets, not vague claims about "operational efficiencies."

Cost synergies (typically 60-80% of total synergy value)

Cost synergies are the more reliable category because you control them directly. Decomposing them works best with a driver tree that breaks the combined cost base into its discrete components before estimating savings, and the levers themselves mirror a standalone cost reduction case. When you have more synergy ideas than the integration team can execute at once, sequence them with an impact-effort matrix so the quick, high-value wins land first. Common sources:

How to estimate in an interview: If the interviewer gives you combined G&A of $200M and tells you 30% of functions overlap, a reasonable cost synergy estimate is $200M x 30% overlap x 20% reduction = $12M in annual run-rate savings. Always state your assumptions explicitly.

Revenue synergies (typically 20-40% of total synergy value)

Revenue synergies are harder to capture and take longer to materialize. Be conservative. Sources include:

- Cross-sell: selling the acquirer's products to the target's customer base (or vice versa). Typical attach rate: 10-25% of the addressable customer base.

- Channel access: using the target's distribution network for the acquirer's products.

- Pricing power: post-merger market share may allow reduced discounting or price increases of 1-3%.

- Product bundling: combining complementary products into higher-value packages.

One-time integration costs

Every synergy comes with upfront costs to capture it. Do not forget to include:

- Severance and restructuring charges (typically 1-2x annual salary for affected headcount)

- IT migration and systems integration ($5-50M depending on complexity)

- Rebranding and customer communication

- Retention bonuses for key talent you want to keep

- Consulting and advisory fees for integration planning

A common rule of thumb: one-time integration costs typically equal 1-2 years of the annual synergy value. If you model $30M in annual synergies, expect $30-60M in integration costs.

Step 4: Integration Risk and Regulatory Analysis

This step separates interview candidates who think about deals on paper from those who think about deals in practice.

Integration risk categories

Cultural fit. This is the single most underestimated risk in M&A. A McKinsey 7S assessment of both organizations reveals structural and cultural mismatches that pure financial due diligence misses. If the target is an entrepreneurial, fast-moving startup and the acquirer is a process-heavy Fortune 500, expect talent attrition of 20-40% in the first 18 months. According to McKinsey's research on cultural integration in M&A, companies that manage culture effectively in their integration planning are around 50% more likely to meet or exceed their synergy targets. Harvard Business Review's M&A research corroborates this finding. That talent attrition can destroy the very capability you acquired.

IT systems integration. Merging ERP systems, CRM platforms, and data architectures is expensive and slow. Failed IT integration has derailed major mergers (Hershey's SAP implementation during a 1999 acquisition is a classic case study). In interviews, flag this risk when the target operates on fundamentally different technology.

Customer retention during transition. Customers of the acquired company may churn if service quality drops during integration, if their key account contacts leave, or if they fear the larger acquirer will deprioritize them. Estimate a customer attrition rate of 5-15% in year 1 and factor that into your revenue projections.

Key talent retention. If the target's value is primarily in its people (common in tech, professional services, and healthcare), you need retention packages. Typical retention bonuses: 50-100% of annual salary for critical employees, vesting over 2-3 years.

Regulatory and antitrust considerations

A SWOT analysis of the combined entity helps surface regulatory exposures alongside internal capabilities before you build the full antitrust argument. For any acquisition that significantly increases market concentration, flag antitrust risk. The quick test:

- Post-merger market share above 30-40% in any relevant market will attract regulatory scrutiny in the US (FTC/DOJ) and EU (European Commission).

- HHI increase above 200 points in a market with HHI above 2,500 is presumed to enhance market power under US DOJ guidelines.

- Remedies may include divesting overlapping business units, licensing IP, or behavioral commitments (pricing, access).

- Timeline impact: antitrust review adds 3-12 months to deal closure. In some industries (telecom, media, healthcare), it can take 18+ months.

In an interview, you do not need to calculate HHI precisely. But if the case involves two large competitors merging, you should proactively flag: "One risk I would want to evaluate is whether the combined market share triggers antitrust review, which could delay the deal or require divestitures that reduce the synergy value."

Step 5: Valuation and Recommendation

Valuation approaches for case interviews

You need to know three valuation methods. Interviewers will not ask you to build a full DCF model in 30 minutes, but they expect you to understand the logic and apply simplified versions.

1. Comparable company multiples (trading multiples)

Look at how the public market values similar companies. The most common metric is EV/EBITDA.

- Find 3-5 comparable public companies in the same industry

- Calculate their EV/EBITDA multiples

- Apply the median or mean multiple to the target's EBITDA

- Example: if comparable companies trade at 8-10x EBITDA and the target has $50M EBITDA, the implied enterprise value is $400-500M

2. Precedent transaction multiples

Look at what acquirers have actually paid for similar companies. These multiples are typically higher than trading multiples because they include a control premium (usually 20-40%).

- If recent acquisitions in the space were done at 10-13x EBITDA, that gives you a range for what the market has accepted as a fair acquisition price

- Precedent transactions are especially useful when the interviewer mentions comparable deals

3. Simplified DCF logic

In an interview, you will not build a full discounted cash flow model. A cost-benefit analysis framework can scaffold the logic: compare the present value of synergy benefits against one-time integration costs to confirm the deal creates net value. In full form, you should understand the concept: the target is worth the present value of its future free cash flows.

- Estimate annual free cash flow (EBITDA minus capex minus taxes, simplified)

- Apply a discount rate (10-12% for most cases, representing the acquirer's cost of capital)

- Quick shorthand: a business generating $40M in annual free cash flow, growing at 3%, discounted at 10%, is worth roughly $40M / (10% - 3%) = $571M using a perpetuity growth model

Payback period

This is the metric interviewers love because it is practical. How many years until the synergies pay back the acquisition premium?

Payback period = (Acquisition premium + Integration costs) / Annual net synergies

If you are paying $600M for a company with a standalone value of $450M, your acquisition premium is $150M. Add $40M in integration costs. If annual net synergies are $50M, the payback period is ($150M + $40M) / $50M = 3.8 years. Most acquirers want a payback under 3-5 years.

Building the recommendation

Use the case interview synthesis format to deliver your recommendation:

Worked Example: Healthcare Software Acquires Analytics Vendor

Case prompt: MedCore, a $400M-revenue regional healthcare software company, is considering acquiring DataPulse, a niche clinical analytics vendor with $60M in revenue. DataPulse is growing at 15% annually with 25% EBITDA margins. MedCore's board wants your recommendation: should they acquire, and at what price?

A. Strategic rationale

MedCore sells electronic health record (EHR) software to mid-size hospital systems. Their customers have been asking for embedded analytics capabilities for two years. MedCore's options:

- Build: 2-3 year development timeline, $25-35M investment, uncertain product-market fit

- Partner: DataPulse or a competitor. Shared economics, limited integration, and risk of the partner being acquired by someone else

- Acquire DataPulse: immediate product gap closure, access to DataPulse's 120-person data science team, and ability to embed analytics natively into MedCore's EHR platform

Verdict: acquisition is the strongest option. The capability gap is urgent (customers are evaluating competitors with analytics), the build timeline is too slow, and a partnership leaves MedCore exposed if DataPulse gets acquired by a rival.

B. Target attractiveness

C. Synergy quantification

Cost synergies: $8M annually

- Headcount reduction in overlapping G&A (finance, HR, legal, office admin): combined G&A of $45M, ~20% overlap, 15% reduction = $1.4M

- Procurement consolidation (cloud hosting, software licenses): combined spend of $35M, 10% savings = $3.5M

- Facility consolidation (DataPulse's HQ lease expires in 14 months, relocate into MedCore campus): $2.1M

- Shared sales operations and marketing infrastructure: $1.0M

Revenue synergies: $12M annually (gross), $8M after haircut

- Cross-sell analytics to MedCore's existing 200 hospital customers: 25% attach rate x $40K average contract = $2.0M in year 1, scaling to $6.0M by year 3

- Bundle pricing uplift on new MedCore deals (analytics adds 15% to contract value): $4.0M at scale

- Channel access: DataPulse's 45 customers become leads for MedCore's EHR: $2.0M at scale

- Apply 30% haircut for execution risk on revenue synergies: $12M x 0.70 = $8.4M, round to $8M

Total annual run-rate synergies: $16M ($8M cost + $8M revenue)

One-time integration costs: $22M

- IT systems integration (merging DataPulse analytics into MedCore EHR platform): $10M

- Severance for redundant positions: $4M

- Retention bonuses for top 30 engineers and data scientists (50% of salary, 2-year vest): $6M

- Rebranding and customer communication: $2M

D. Valuation and price range

Comparable company multiples:

- Healthcare IT companies trade at 12-16x EBITDA

- DataPulse EBITDA: $15M

- Standalone value range: $180M to $240M

Precedent transactions:

- Recent healthcare analytics acquisitions closed at 14-18x EBITDA (reflecting premium for fast-growing analytics businesses)

- Implied range: $210M to $270M

Synergy-adjusted maximum price:

- Standalone midpoint: $210M

- Present value of synergies (5 years of $16M annual synergies, discounted at 10%): approximately $61M

- Integration costs: $22M

- Maximum price the acquirer should pay: $210M + $61M - $22M = $249M

- This implies paying roughly 16.6x current EBITDA, within the precedent transaction range

E. Payback period

- Acquisition premium over standalone midpoint: $249M - $210M = $39M (if paying maximum price)

- Integration costs: $22M

- Total incremental investment to justify: $61M

- Annual net synergies (once fully captured, year 3+): $16M

- Payback period: $61M / $16M = 3.8 years

A payback under 4 years is reasonable for a strategic acquisition in healthcare IT. If MedCore can negotiate the price down to $230M, payback drops to about 2.6 years, which is excellent.

F. Key risks

G. Recommendation

"I recommend MedCore proceed with the DataPulse acquisition at a target price of $220-240M, representing 14.7-16.0x EBITDA. The deal closes a critical product gap in clinical analytics, generates an estimated $16M in annual synergies against $22M in one-time integration costs, and pays back in approximately 3-4 years. The primary risk is talent retention of DataPulse's engineering team. I would mitigate this with pre-announced retention packages and an autonomy charter. Before signing, I would prioritize due diligence on customer contract transferability and the IT integration roadmap."

M&A · medium

Practice a live M&A case end-to-end

Healthcare / Digital Health

How M&A Relates to Other Frameworks

M&A cases do not exist in isolation. In most interviews, you will pull elements from adjacent frameworks. Understanding the overlap helps you flex your structure based on what the prompt emphasizes.

The key skill is recognizing when to pivot. If the interviewer's follow-up questions focus on the target's margin decline, shift into profitability framework mode. If they ask about entering a new market through the acquisition, apply market entry logic. The frameworks are tools, not scripts.

What are the most common M&A case mistakes?

The most common M&A case mistakes are jumping to a "yes" without testing build or partner alternatives, making vague synergy claims, ignoring integration costs, underweighting culture and talent risk, skipping valuation guardrails, and forgetting regulatory risk. Each one below shows up repeatedly in MBB second-round interviews.

- Jumping to "yes, acquire" without testing alternatives. Always evaluate build and partner options first. Interviewers specifically test whether you default to the most expensive option.

- Vague synergy claims. Saying "there would be cost synergies" without quantifying them is not analysis. Give dollar estimates with explicit assumptions.

- Ignoring integration costs. Synergies sound great until you subtract the $20-50M it takes to capture them. Always net out one-time costs.

- Overlooking cultural and talent risk. Especially in capability-driven acquisitions (tech, professional services), the value walks out the door if key people leave.

- No valuation guardrails. Recommending "acquire" without stating a price range means you have not actually answered the question. Always state the maximum price you would support.

- Forgetting regulatory risk. In consolidation deals, antitrust review can block or significantly delay the transaction. Flag this proactively when market shares are high.

Interactive M&A Drills

Sources and Further Reading (checked June 17, 2026)

- McKinsey, "Where mergers go wrong," revenue synergy failure research: mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights/where-mergers-go-wrong

- McKinsey, "The importance of cultural integration in M&A": mckinsey.com/industries/oil-and-gas/our-insights/the-importance-of-cultural-integration-in-m-and-a-the-path-to-success

- McKinsey, M&A strategy and corporate finance insights: mckinsey.com/capabilities/strategy-and-corporate-finance/our-insights

- Bain, M&A report and merger integration research: bain.com/insights/topics/m-and-a-report

- Bain, M&A capability and integration playbook: bain.com/consulting-services/mergers-acquisitions

- BCG, corporate development and M&A strategy: bcg.com/capabilities/corporate-finance-strategy

- Harvard Business Review, "The Big Idea: The New M&A Playbook" (M&A failure rate): hbr.org/2011/03/the-big-idea-the-new-ma-playbook

- Harvard Business Review, "M&A: The One Thing You Need to Get Right": hbr.org/2016/06/ma-the-one-thing-you-need-to-get-right

- Harvard Business Review, M&A topic archive: hbr.org/topic/mergers-and-acquisitions

- IGotAnOffer, how to master M&A consulting case studies: igotanoffer.com/blogs/mckinsey-case-interview-blog/merger-and-acquisition-cases

- PrepLounge, M&A case type overview: preplounge.com/en/case-interview-basics/ma

- PrepLounge, how to solve M&A consulting case studies: preplounge.com/en/case-interview-basics/case-cracking-toolbox/identify-your-case-type/mergers-and-acquisitions

- Management Consulted, case interview types and M&A frequency data: managementconsulted.com/case-interview-types

- US DOJ and FTC, Horizontal Merger Guidelines (2023 revision): justice.gov/atr/merger-enforcement

Related Guides

- Case Interview Frameworks Complete Guide, the master framework selector with worked examples across all major case types

- PE Due Diligence Framework, adds financial return analysis and portfolio company value creation to the M&A lens

- Value Chain Framework, maps where cost and revenue synergies actually live across operations

- Growth Strategy Cases, the revenue growth logic that informs whether a target adds strategic optionality

- Cost Reduction Case Interview, for building the cost synergy side of the deal model

- Market Entry Framework

- Profitability Framework

- Case Interview Synthesis

- How to Practice Case Interviews

FAQ

Frequently asked questions

Keep reading

- Start free consulting drillsPractice

- 3Cs Framework: Company, Customer, Competitor (Worked Example)Frameworks · Feb 6, 2026

- 4Ps Framework Case Interview: Product, Price, Place, PromotionFrameworks · Feb 6, 2026

- Ansoff Matrix vs BCG Matrix for Case InterviewsFrameworks · Jun 2, 2026

- Porter's Five Forces for Case Interviews: How to Analyze Industry AttractivenessFrameworks · Feb 6, 2026

- PE Due Diligence Framework for Case Interviews (2026)Frameworks · Feb 19, 2026