Real Estate Case Interview: Framework, Metrics, and Worked Example (2026)

Master real estate case interviews with cap rate, NOI, IRR, DCF, core case types, and a worked REIT portfolio optimization example.

On this page

A real estate case interview tests whether you can evaluate a property strategy decision - market entry, valuation, portfolio optimization, or build/buy/lease - using the metrics that drive real estate recommendations. The important move is not memorizing a global market-size number. It is translating cap rate, NOI, IRR, DCF, lease terms, and submarket risk into an executive recommendation. This guide covers the metrics, the frameworks, the four case archetypes, and a worked REIT portfolio optimization.

Real Estate Consulting vs. Real Estate Finance: What's the Difference?

This distinction trips up more candidates than any other concept in real estate interviews. Confusing the two leads to over-engineering the analytics in a consulting case, or under-structuring the decision in a finance interview.

Real estate consulting cases test strategic judgment. You are advising a developer, REIT, or institutional investor on a decision: should they enter a new market, acquire an asset, optimize a portfolio, or restructure a lease? The deliverable is a structured recommendation backed by key metrics. You will reference cap rates, NOI, and IRR, but you will not be expected to build a 10-tab DCF model during the interview.

Real estate finance interviews test technical modeling. You will be asked to build a DCF in Excel, calculate DSCR (Debt Service Coverage Ratio), or value an asset using comparable transaction multiples. The deliverable is analytical precision, not strategic framing.

As a practical rule of thumb: consulting = structure the decision; finance = build the model.

At McKinsey and BCG, real estate cases may arise when advising pension funds, sovereign wealth funds, or large developers on portfolio strategy. At CBRE and JLL, cases often sit closer to advisory mandates: market entry feasibility, asset repositioning, or location strategy for occupiers. At real estate PE firms, the cases can blend both, but the interview style often leans finance unless you are interviewing for a strategy or portfolio management role.

For a broader view of how to orient your preparation across firm types, see the management consulting firms ranking guide.

Who Gives Real Estate Case Interviews

Real estate cases appear across a wider range of employers than most candidates expect.

Large real estate advisory firms use data platforms, market benchmarking, and submarket research heavily. Knowing this shapes how you frame analytical methods during your recommendation: use market comparables, leasing data, vacancy, rent growth, and capex assumptions rather than generic "market attractiveness" language.

Four Core Real Estate Metrics

Master these four metrics before any real estate case. Cap rate is usually the fastest comparator across markets and asset classes, but it is only useful when paired with the quality of NOI and the risk behind the asset.

1. Cap Rate (Capitalization Rate)

Formula: Cap Rate = NOI / Asset Value

A $5M office building generating $500K annual NOI has a 10% cap rate. Cap rate compresses (falls) when market demand rises and asset values increase faster than income. A 4% cap rate in Manhattan's Class A office market versus a 9% cap rate in a secondary Midwest market reflects the risk-return differential between the two.

In a case, use cap rate to: (a) compare yield across markets or asset classes, (b) back-solve for implied asset value given a market cap rate, or (c) assess whether a target acquisition is priced fairly relative to comparables.

2. NOI (Net Operating Income)

Formula: NOI = Gross Rental Revenue − Operating Expenses (excluding debt service and taxes)

NOI is the income a property generates before financing costs. It is the numerator in the cap rate formula and the foundation for DCF projections. In a case, always distinguish between NOI today and stabilized NOI. A value-add asset may have a low current NOI due to vacancy, with a much higher stabilized NOI once the asset is repositioned.

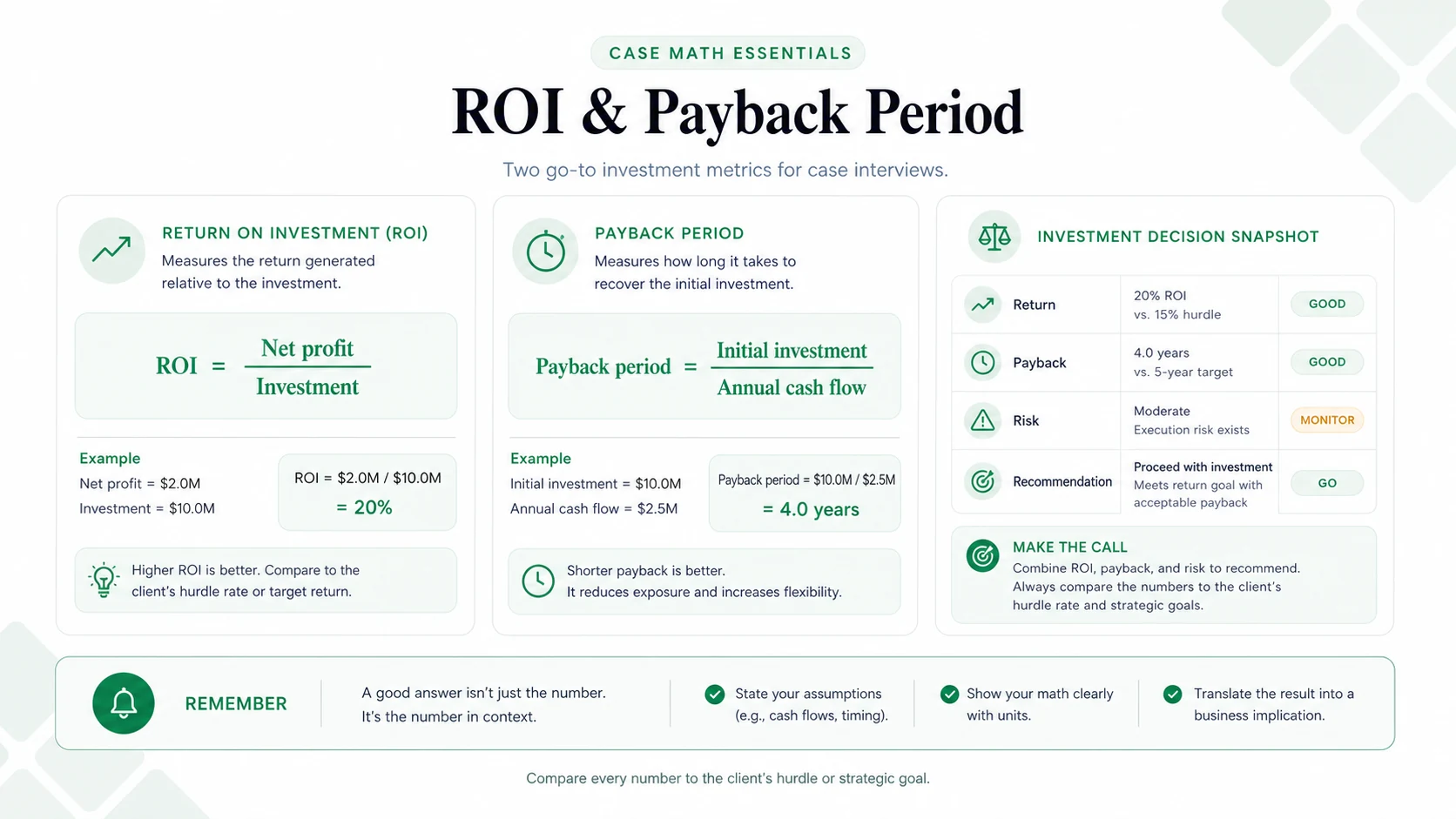

3. IRR (Internal Rate of Return)

IRR is the annualized return that makes the net present value of all cash flows (including exit proceeds) equal to zero. In real estate consulting cases, IRR is the primary metric for comparing investment alternatives across different holding periods and capital structures. A 10-year hold with a 7% levered IRR is directly comparable to a 5-year hold with a 12% levered IRR. A consultant's job is to frame which is more appropriate given the client's investment mandate.

4. DCF (Discounted Cash Flow)

DCF translates future NOI streams and an exit value (based on terminal cap rate) into a present value. In consulting cases, you will rarely build a full DCF, but you need to articulate what drives value: NOI growth assumptions, terminal cap rate, holding period, and discount rate. The most common consulting ask is: "What assumptions would need to hold for this acquisition to meet a 12% IRR hurdle?"

The Four Core Real Estate Case Types

Real estate consulting cases often cluster into four archetypes. Identifying the likely type early lets you deploy the right sub-framework quickly.

1. Market Entry: Should our client (a developer, REIT, or retailer) enter Market X? Evaluate: market demand drivers, competitive supply, regulatory environment, capital requirements, and expected returns (cap rate benchmarks, IRR projections). Use the market entry framework as the spine, then layer in real estate-specific metrics.

2. Asset Valuation: What is this property worth, and at what price does the deal make sense? Approach via two methods: income approach (NOI / target cap rate = implied value) and comparable transaction analysis (price per square foot benchmarked to recent sales). Always triangulate both. If they diverge, explain why.

3. Portfolio Optimization: The client holds 40 assets across 6 markets. Which should they hold, which should they sell, and which should they reposition? Score each asset on two dimensions: income quality (NOI stability, lease term, tenant credit) and capital appreciation potential (market growth, cap rate compression outlook). Assets that score low on both dimensions are disposal candidates.

4. Build / Buy / Lease (Space Strategy): Should the client build a new facility, acquire an existing one, or lease? Compare total cost of ownership across the relevant horizon: build (capex + ongoing opex), buy (acquisition cost + capex + opex, offset by terminal value), and lease (annual rent escalated + no terminal value). This is a common real estate case type at Big 4 advisory firms advising corporate occupiers.

For M&A-adjacent real estate cases (e.g., valuing a property-owning company), the M&A case framework provides complementary structure.

Framework: Market Entry for a Property Developer

When a developer asks whether to enter a new city or asset class, structure the analysis in five layers.

Framework

Real Estate Market Entry Framework

- 01

1. Demand Assessment

Population growth, employment base, income levels, household formation rate. Is demand structural (demographics) or cyclical (economic boom)?

- 02

2. Supply Analysis

Current vacancy rate, pipeline of new supply, construction cost trends, barriers to entry (land scarcity, zoning, permitting timelines). High supply pipeline = cap rate risk.

- 03

3. Competitive Landscape

Who are the dominant developers and landlords? What is their typical product? Is there a quality gap the client can exploit?

- 04

4. Financial Feasibility

Land cost + construction cost + financing cost vs. stabilized NOI and exit value. What cap rate is the market pricing? What IRR does the project deliver at that cap rate?

- 05

5. Risk and Mitigants

Regulatory risk (zoning changes, rent control), macro risk (interest rate sensitivity), execution risk (construction cost overruns, lease-up timeline). For each risk, what is the mitigant?

The most common interviewer push-back in a market entry case: "You've shown the market is attractive, but why should OUR CLIENT enter, and why now?" Answer by connecting client-specific capabilities (balance sheet, development expertise, existing tenant relationships) to the market opportunity.

Framework: Real Estate Valuation Cases

For asset-level valuation, use a two-method approach and reconcile the results.

Income Approach:

- Determine current and stabilized NOI (adjust for vacancy, lease expiry, capex requirements)

- Apply market cap rate to stabilized NOI → implied value

- Sensitivity: at what cap rate does the deal break (IRR falls below hurdle)?

Comparable Transaction Analysis:

- Identify 3-5 recent transactions in the same submarket, similar asset class and quality

- Calculate price per square foot or price per unit (multifamily)

- Adjust for quality differences and market timing

Reconciliation: If income approach yields $50M and comparables suggest $45M, the premium is justified only if stabilized NOI assumptions are achievable. Test the key assumptions explicitly.

For cases involving distressed assets or value-add repositioning, also calculate the "as-is" value (current NOI, wider cap rate) versus the "stabilized" value (target NOI, compressed cap rate) to frame the value creation thesis.

See PE due diligence framework for the diligence layer that sits above asset valuation when a fund is evaluating a platform acquisition.

Worked Example: REIT Portfolio Optimization

Prompt: "Our client is a U.S. diversified REIT with a $2.4B portfolio spanning 48 assets across four sectors: Office (40%), Retail (25%), Industrial (25%), Multifamily (10%). Total portfolio NOI is $144M (6% blended cap rate). The CEO wants to improve ROIC from 6% to 8% within 3 years. What would you recommend?"

Step 1: Anchor the gap.

Target NOI at 8% ROIC on $2.4B = $192M. Current NOI = $144M. Gap = $48M. The question is whether the gap is better closed by: (a) selling low-yield assets and redeploying capital, (b) repositioning underperforming assets, or (c) acquiring higher-yield assets.

Step 2: Diagnose by sector.

Step 3: Identify reallocation levers.

The Office portfolio at 5.0% cap rate and declining fundamentals is the portfolio drag. Industrial at 7.0% cap rate with structural tailwinds is the growth engine.

Lever 1: Dispose of Class B office. Assume $300M of the $960M Office portfolio is Class B with 18% vacancy and a deteriorating NOI outlook. If those assets generate $15M NOI and buyers underwrite them at a 5.5% exit cap rate, implied sale value is $15M / 5.5% = approximately $272M. That gives the client capital to redeploy, but it also crystallizes the discount from weaker office fundamentals.

Lever 2: Redeploy into Industrial. Assuming the $272M is redeployed into logistics assets at a 7.5% going-in cap rate, it generates about $20.4M in NOI. In a real interview, state that this is a case assumption and ask for comparable transactions to pressure-test it.

Lever 3: Reposition Class B Multifamily to Sun Belt. Exit $120M of flat-NOI gateway multifamily at a 5.2% cap rate ($6.24M NOI implies $120M value), then redeploy into Sun Belt multifamily at a 5.8% going-in cap rate with a modest rent-growth assumption. The recommendation depends on whether those rent-growth and lease-up assumptions survive diligence.

Year 3 NOI projection:

Gap remaining: $192M target minus $162M projected = $30M still short. The recommendation must address this: "The reallocation moves ROIC from 6.0% to approximately 6.75% by Year 3. Reaching 8% within 3 years requires either additional asset recycling, an acquisition of a higher-yield platform, or relaxing the timeline to 5 years if transaction liquidity is constrained."

Synthesis: "I recommend a two-phase portfolio rotation. Phase 1: dispose of Class B Office and selected gateway Multifamily assets; redeploy into logistics Industrial and higher-growth Multifamily markets. This improves blended ROIC but does not fully close the gap. Phase 2: evaluate a bolt-on acquisition or additional asset rotation to reach the 8% target. The target is directionally achievable, but likely on a longer timeline unless the client accepts more transaction and execution risk."

Common Mistakes in Real Estate Cases

Ignoring capital expenditure in NOI. NOI excludes capex, but capex matters enormously in asset valuation and portfolio optimization. A building requiring $20M in near-term capex has a lower effective yield than its nominal cap rate suggests. Adjust for capex in any valuation recommendation.

Applying a single cap rate across asset classes. Office, industrial, retail, and multifamily trade at very different cap rates in the same market. Using a blended 6% cap rate for a mixed portfolio will give the wrong answer on any sector-level analysis.

Forgetting the exit. Real estate returns are partly driven by cap rate compression on exit (buying at 7% today, selling at 5.5% in 5 years when the market matures). In an IRR analysis, always state your exit cap rate assumption explicitly and test sensitivity: "At a 6% exit cap rate instead of 5.5%, what happens to IRR?"

Over-anchoring on national trends. Real estate is local. A national multifamily oversupply narrative may not apply to a specific Sun Belt submarket with constrained land supply. Always push for submarket data.

For frameworks that sit adjacent to real estate cases, the profitability framework applies when real estate is a cost line in a broader corporate case, and the growth strategy cases guide covers geographic expansion decisions that often trigger a build/buy/lease analysis.

30-Day Real Estate Case Prep Plan

Checklist

Execution checklist

Week 1: Master the four metrics (cap rate, NOI, IRR, DCF)

These appear in every real estate valuation case. Be able to define, calculate, and interpret each in under 60 seconds.

Week 1: Practice cap rate math in 30 seconds flat

Interviewers expect instant recall. Given NOI = $750K and cap rate = 7.5%, solve for asset value ($10M). Do 20 reps until it's reflexive.

Week 2: Practice one Market Entry case with the 5-layer framework

Market entry is the most common real estate consulting case type. Drill demand, supply, competitive, financial, and risk layers.

Week 2: Practice one Portfolio Optimization case using the 2x2 scoring matrix

Income quality vs. capital appreciation potential: be fluent in ranking assets and making disposal/hold/reinvest recommendations.

Week 3: Practice the Build/Buy/Lease case type

Common at Big 4 and corporate strategy roles. Build a 10-year total cost of ownership comparison from memory.

Week 3: Study one real REIT's annual report (e.g., Prologis, Equity Residential)

Reading an actual REIT's MD&A builds intuition for how cap rate, NOI, and portfolio strategy language is used in practice.

Week 4: Run 3+ timed mock cases under interview conditions

Structuring under time pressure with an interviewer probing assumptions is a skill that requires repetition, not just content knowledge.

Week 4: Review the consulting interview prep timeline to stress-test your schedule

Ensure real estate prep integrates with broader case and behavioral prep. Candidates who over-index on technical metrics and under-prepare behaviors lose offers.

For the broader context of how real estate prep fits into a full consulting interview timeline, see the consulting interview prep timeline guide.

Related Guides

- PE Due Diligence Framework: the diligence layer above asset-level valuation in PE real estate cases

- Financial Services Case Interview: relevant when the client is a REIT, insurance company, or pension fund with real estate holdings

- ESG Sustainability Case Interview: green building standards, energy efficiency retrofits, and climate risk in property portfolios

- Government and Public Sector Case Interview: zoning, permitting, and public housing cases where government is the counterparty or regulator

- Energy Case Interview: site acquisition for solar, wind, and data-center power infrastructure frequently appears as real estate strategy

- M&A Case Framework: applies when the case involves acquiring a property-owning company or platform

Sources and Further Reading (checked June 17, 2026)

- Grand View Research, Real Estate Consulting Market Size & Forecast 2025–2034: grandviewresearch.com/industry-analysis/real-estate-consulting-market

- JLL, Global Real Estate Outlook 2025: jll.com/en/trends-and-insights/research/global-real-estate-outlook

- CBRE, U.S. Cap Rate Survey 2025: cbre.com/insights/reports/us-cap-rate-survey

- Hacking the Case Interview, Investment Case Interview: hackingthecaseinterview.com/pages/investment-case-interview

- NAREIT, U.S. REIT Industry Fact Sheet 2025: reit.com/data-research/reit-market-data/us-reit-industry-equity-market-cap

- Cushman & Wakefield, Global Office Market Report 2025: cushmanwakefield.com/en/insights/global-office-report

FAQ

Frequently asked questions

Keep reading

- Airline Case Interview: Profitability Framework, Revenue Drivers, and Worked Examples (2026)Frameworks · Mar 29, 2026

- Ansoff Matrix Case Interview: The 2x2 Growth Framework Explained with ExamplesFrameworks · Mar 25, 2026

- BCG Matrix Explained: Stars, Cash Cows, Question Marks, Dogs (2026)Frameworks · Mar 25, 2026

- Healthcare Case Interview: Framework, Key Questions, and Worked Examples (2026)Frameworks · Mar 25, 2026