Alvarez & Marsal Case Interview: Restructuring Cases, Format, and Prep Guide (2026)

Alvarez & Marsal case interviews are candidate-led with a focus on restructuring, liquidity, and performance improvement. Learn the format and 30-day prep plan.

On this page

Alvarez & Marsal runs candidate-led case interviews with a heavy emphasis on restructuring, liquidity analysis, and operational turnaround, not the market entry and growth strategy cases you'd encounter at McKinsey or BCG. The process runs 2–3 rounds: a behavioral-heavy first round followed by a second round of 3–6 back-to-back interviews that blend cases and behavioral questions, often ending with a networking lunch or dinner. Cases are 30–60 minutes total with 20–35 minutes of active case work, and you are expected to drive direction, request data proactively, and apply finance-heavy frameworks including 13-week cash flow modeling and capital structure analysis.

Alvarez & Marsal Interview Format: Rounds, Timeline, and What to Expect

The A&M interview process is structured differently from MBB. The first round is behavioral-dominant: A&M wants to assess fit and operational mindset before investing time in case evaluation. The case intensity builds in the second and third rounds.

Campus recruiting timelines run September–November for full-time and November–February for summer internships. Off-cycle hiring moves faster. A&M's careers page confirms that the process averages approximately one month from application to offer.

Framework

A&M Interview Process

- 01

Application + Screening

Resume review. Some offices require an online numerical/verbal assessment (25–40 min). Not universal; check your invitation. Campus recruiting skips the recruiter phone screen.

- 02

Round 1: Behavioral-Heavy

1–2 interviews focused on behavioral questions, fit, and why A&M / restructuring. May include a short case or case-related discussion. Primarily tests communication and motivation.

- 03

Round 2: Case + Behavioral Mix

3–6 back-to-back interviews, each 45–60 minutes, mixing candidate-led case interviews with behavioral questions. Held on-site (Super Day format) or virtually. This is where most candidates are evaluated on case performance.

- 04

Round 3 / Networking

Senior partner or MD-level interviews. Often includes a networking lunch or dinner. Cultural fit and commercial judgment are heavily weighted at this stage.

- 05

Offer

Typically within 1–2 weeks of final round. Some offices provide limited feedback to unsuccessful candidates upon request.

How A&M Cases Differ from MBB

The single most important thing to understand before walking into an A&M interview: this is not McKinsey. The case types, the expected analytical depth, and the format all reflect A&M's operational DNA.

Candidate-Led, Not Interviewer-Led

A&M uses candidate-led case interviews. Unlike the McKinsey-style where the interviewer walks you through specific questions in a structured sequence, A&M expects you to independently structure the problem, decide which areas to prioritize, request data proactively, and synthesize findings without prompting. When you finish presenting your framework, the interviewer waits. You drive the next move.

This is a meaningful difference in practice. Candidates who trained heavily on McKinsey-style cases often pause and look at the interviewer after presenting their structure. That pause is scored as passivity at A&M. You need to say, "I'd like to start with the liquidity analysis because in a distressed situation, cash runway is the most urgent constraint. Can I see the current cash balance and the weekly burn rate?" and move forward.

For a detailed breakdown of how candidate-led interviews differ mechanically, see case interview frameworks complete guide.

Finance-Heavy, Not Strategy-Heavy

MBB cases are designed for generalists who will staff across industries. A&M cases are designed for consultants who will parachute into distressed situations and immediately contribute to financial analysis. Expect:

- Liquidity analysis: How many weeks of cash does the company have? What's the burn rate? Can they make payroll next quarter?

- Profitability diagnosis: Where exactly is the margin erosion? Is it gross margin, SG&A, or both?

- Capital structure: Is the company insolvent (liabilities > assets) or illiquid (cash flow negative)? That distinction matters for what actions are available.

- Cost optimization: Which cost lines can be cut without destroying revenue-generating capacity?

- 13-week cash flow modeling: A&M's signature tool for managing distressed companies through restructuring engagements.

For background on the profitability framework that underpins many A&M cases, see profitability framework. For M&A-related case types, see M&A case framework.

Practice this next: Run a free restructuring-style case and force yourself to start with cash runway before moving to EBITDA, debt capacity, or operational fixes.

Operational, Not Advisory

A&M consultants often take interim executive roles (CFO, COO, CRO) inside client companies. The cases reflect this: you're not advising the CEO from the outside, you're operationalizing a solution from the inside. That shifts the framing from "what should they do" to "how would you actually do it, and what could go wrong."

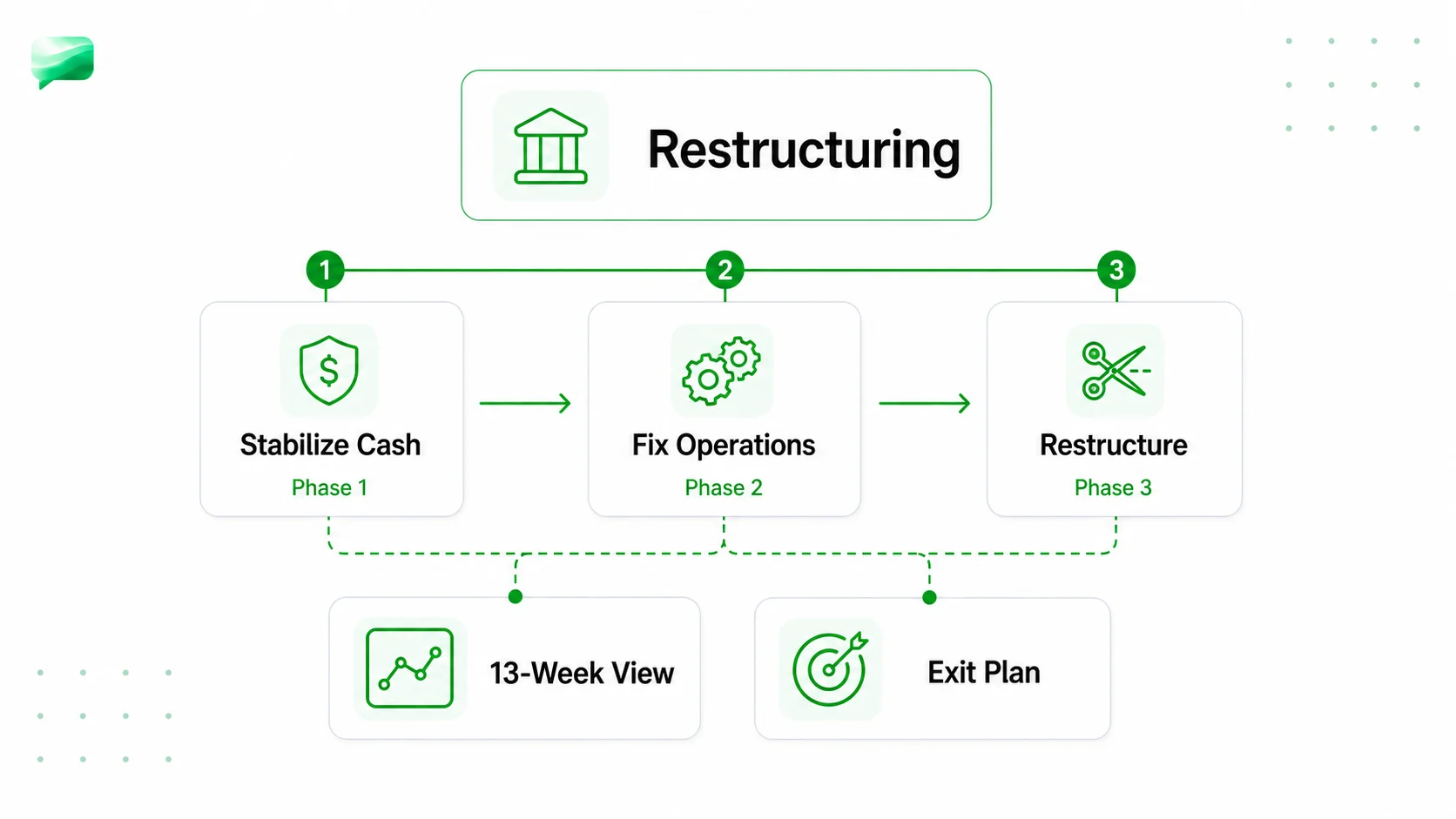

The A&M Restructuring Case Framework

Generic consulting frameworks (3Cs, Porter's Five Forces, standard profitability trees) are insufficient for A&M restructuring cases. You need a turnaround-specific structure that reflects how distressed situations actually work.

The core A&M restructuring framework operates in three phases:

Phase 1: Stabilize Cash (Immediate, 0–13 Weeks)

The first question in any distressed situation is: will the company run out of cash before the restructuring can be executed? Everything else is secondary.

- Cash runway: Current cash balance ÷ weekly cash burn = weeks of runway

- 13-week cash flow forecast: Direct method (weekly receipts minus weekly disbursements). Not EBITDA, not net income. Actual cash in and out.

- Emergency levers: Delay AP payments, accelerate AR collections, sell non-core assets, draw on revolving credit

- Minimum viable liquidity: What cash balance must be maintained to keep operations running (payroll, critical vendors, leases)?

Phase 2: Fix the Business (Medium-Term, 3–18 Months)

Once the cash emergency is stabilized, address the underlying business problems:

- Revenue: Is revenue declining? Why (volume, price, or mix)? Can it be recovered or should capacity be rightsized?

- Cost structure: What is the fixed vs. variable cost breakdown? What can be eliminated without destroying revenue?

- Working capital: Inventory days, receivables days, payables days. Where are the inefficiencies?

- EBITDA bridge: From current EBITDA to target EBITDA, quantify each lever

Phase 3: Restructure the Balance Sheet (Concurrent or Following)

- Debt capacity: Based on stabilized EBITDA and cash flow, how much debt can the business service?

- Creditor negotiation: What do secured vs. unsecured creditors get in a restructuring scenario?

- Options: Out-of-court restructuring, Chapter 11 reorganization, or sale process (363 sale)?

- Stakeholder management: Lenders, suppliers, employees, and customers all have different interests and different leverage

For a deeper treatment of restructuring case structures, see restructuring case interview.

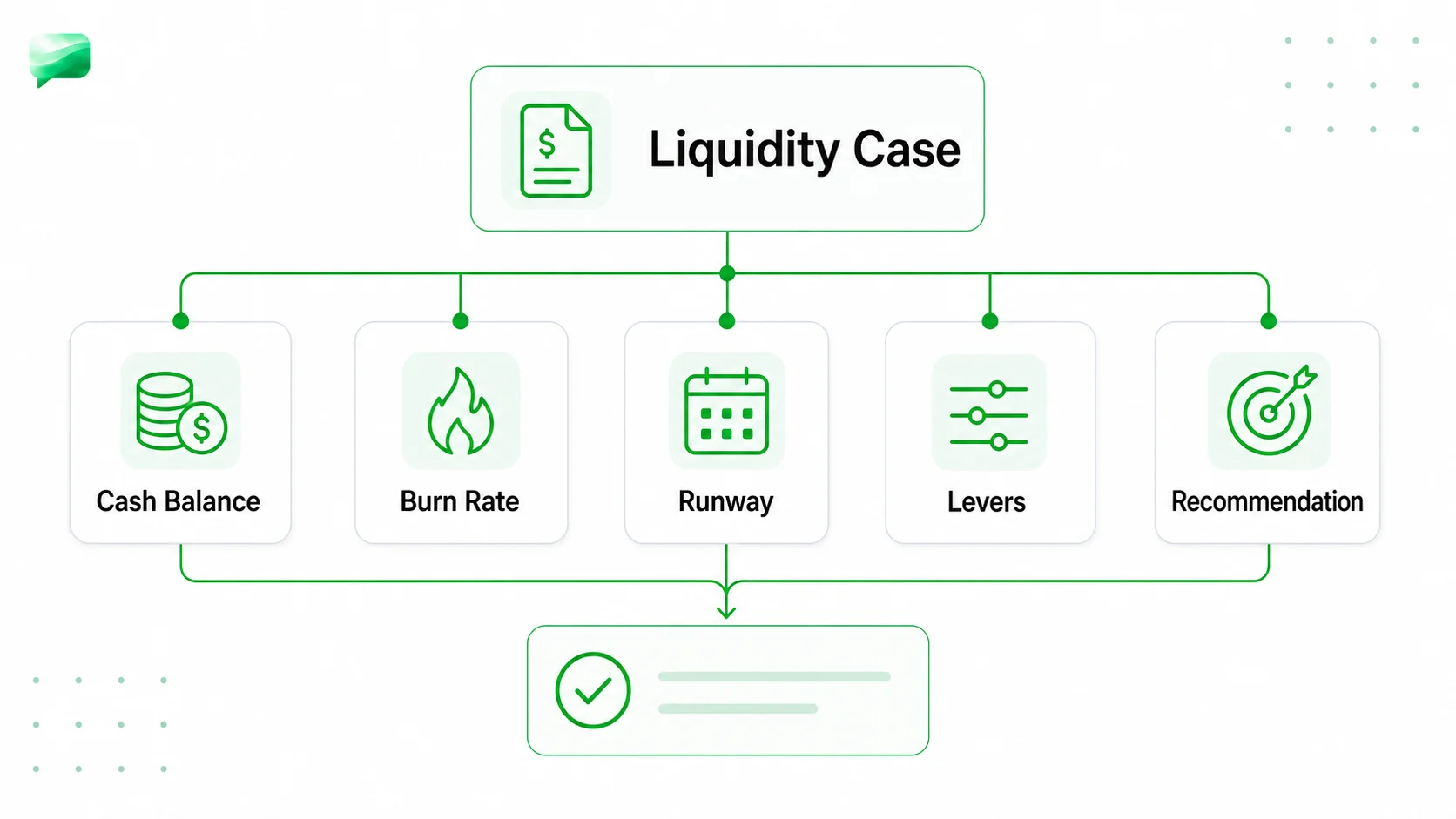

Worked Example: A&M-Style Liquidity and Cash Flow Case

This example reflects the type of quantitative case you should expect in a Round 2 A&M interview.

Profitability · medium

Practice an A&M-style margin recovery case

Consumer Packaged Goods / Beverages

Case Prompt: Your client is a mid-sized specialty retailer with $180M in annual revenue. Over the past 18 months, EBITDA has declined from $14M to -$2M. The CEO has hired A&M. You've been assigned as the lead. Your first task: assess whether the company can make it to the end of Q2 (14 weeks from now) without a liquidity crisis, and outline the immediate actions.

Data provided when you ask:

Step 1: Calculate cash runway

Current cash: $4.2M Weekly burn: $0.8M Weeks of runway without any action: $4.2M ÷ $0.8M = 5.25 weeks

The company cannot make it to the debt service payment in Week 6. Without intervention, it runs out of cash in approximately 5 weeks.

Step 2: Assess available liquidity levers

Available revolving credit: $2.5M → Total available cash with revolver draw: $4.2M + $2.5M = $6.7M

Weeks of runway with full revolver draw: $6.7M ÷ $0.8M = 8.4 weeks

Still short of the 14-week horizon. Need additional actions.

Step 3: Working capital acceleration

- AR collections acceleration: Can we collect $2M of the $6.4M AR in the next 4 weeks by offering a 2% early payment discount? Cost of discount: $40K. Cash benefit: $2.0M in Weeks 2–4.

- AP extension: Renegotiate $5M of the overdue AP to 90-day terms. Frees up $5M over the next 8 weeks (~$625K/week).

Revised weekly cash position with these actions:

- Weeks 1–4: Burn improves to approximately -$0.2M/week (AP extension reduces disbursements from $3.6M to $3.0M, AR collection adds $0.5M/week)

- Revised runway to Week 14: Starting cash $4.2M + revolver $2.5M + AR $2.0M = $8.7M. Net outflow Weeks 1–14 at improved burn of ~$0.2M/week = $2.8M. Ending cash: $8.7M - $2.8M - $3.0M debt service = $2.9M

The company can reach Week 14 with $2.9M in cash (above minimum viable liquidity) if all three levers are executed.

Step 4: Recommendation

"The company is 5 weeks from a cash crisis at current burn, not 14 weeks. Three immediate actions stabilize the runway: (1) draw the remaining $2.5M revolving credit facility immediately; (2) accelerate AR collections with a 2% early-pay incentive ($2M collected in 4 weeks at a $40K cost); (3) renegotiate overdue AP to 90-day terms ($5M deferred, reducing weekly disbursements by approximately $600K). Together these extend runway to Week 14 with a $2.9M buffer. The key risk is AP vendor refusal; we need to identify which vendors are critical and ring-fence them before the negotiation. Parallel to cash stabilization, I'd want to understand the EBITDA decline to identify the sustainable burn rate post-stabilization."

This is the quality of answer A&M interviewers expect: precise numbers, clear sequencing of levers, a stated recommendation with a risk, and a bridge to the next phase of analysis. For more on structuring synthesis this way, see case interview synthesis.

Practice this next: Use case math drills for runway, burn-rate, and working-capital calculations, then run a free A&M-style turnaround case.

Common Mistakes in A&M Case Interviews

Leading with strategy before establishing cash position. Restructuring cases start with liquidity, not strategy. An 18-month operational improvement plan is useless if the company runs out of cash in Week 6. Anchor in cash before addressing business performance.

Using a generic profitability framework. "Revenue minus costs" is not a restructuring framework. A&M interviewers want to see the Phase 1/2/3 turnaround structure: stabilize cash, fix operations, restructure the balance sheet. Apply a context-specific structure.

Conflating insolvency with illiquidity. These are different problems requiring different solutions. An illiquid company has good long-term prospects but cannot meet near-term obligations; it needs bridge financing or working capital management. An insolvent company has structural liabilities exceeding assets; it may need Chapter 11 or a sale process. Knowing the difference signals finance sophistication.

Ignoring stakeholder dynamics. A&M restructuring engagements involve creditors, lenders, equity holders, employees, and suppliers with conflicting interests. A recommendation that ignores creditor consent requirements or supplier leverage misses a real-world constraint that practitioners think about constantly.

Weak behavioral stories. Round 1 is behavioral-heavy. A&M wants evidence of resilience, leadership in high-pressure situations, and operational judgment. Generic STAR stories about team projects don't resonate; they want stories about navigating ambiguity, making decisions under incomplete information, and driving outcomes with limited resources.

For behavioral interview preparation, see behavioral interview consulting. For a full prep timeline that sequences your preparation intelligently, see consulting interview prep timeline.

30-Day A&M Prep Plan

Checklist

30-Day Alvarez & Marsal Prep Plan

Week 1: Study 13-week cash flow model mechanics and liquidity vs. solvency distinction

Restructuring fundamentals and financial vocabulary are the foundation; A&M expects fluency from Day 1

Week 1: Build behavioral story bank (3 high-pressure decisions, 2 operational problems, 1 failure)

A&M's Super Day format includes behavioral questions between cases; stories must be rehearsed and under 2 minutes

Week 2: Practice candidate-led protocol with 2 profitability cases per day

A&M uses candidate-led format; you drive every transition with no hints or prompts from the interviewer

Week 2: Drill cash runway and working capital calculations (AR days, AP days, inventory days)

Restructuring cases require fast, accurate financial math without a calculator

Week 3: Study M&A diligence types (sell-side, buy-side, distressed 363 sale) and capital structure concepts

A&M's Transaction Advisory practice runs M&A cases alongside restructuring; expect both

Week 3: Complete 3 back-to-back mock interviews in a single sitting (Super Day simulation)

A&M Super Days run 4+ cases consecutively; stamina and consistency matter as much as individual case performance

Week 4: Run 2 full Super Day simulations and close your single weakest dimension

Targeted improvement beats even practice; identify your weakest area from Weeks 1 to 3 and drill it specifically

Week 4: Finalize 5 core behavioral stories and research A&M's recent engagements

Fit questions at A&M test genuine interest in restructuring and operations; generic consulting answers won't land

How A&M Fits Into Your Consulting Prep Strategy

If you're targeting A&M alongside other firms, the content overlap with standard MBB prep is partial, not complete. The candidate-led format transfers from firms like Oliver Wyman. The profitability and cost frameworks transfer from general consulting prep. What doesn't transfer: the restructuring-specific vocabulary, the liquidity-first analytical sequence, and the operational stakeholder framing.

Candidates with investment banking, private equity, or corporate finance backgrounds will find the financial content more familiar than the average MBB-prepped candidate. Candidates with pure strategy consulting backgrounds need to spend deliberate time on the finance fundamentals in Week 1.

A&M is part of a tier of firms (alongside AlixPartners, FTI Consulting, and Kroll) that specialize in situations-based advisory rather than pure strategy. To understand how A&M's restructuring focus compares to other consulting firm types, it helps to map where turnaround advisory sits next to strategy, operations, and Big 4 practices. The interview prep logic is different: you're not learning to impress a generalist interviewer with elegant frameworks, you're demonstrating that you can operate effectively inside a distressed company under time pressure.

For the framework skills that underpin strong A&M performance, review case interview frameworks complete guide and restructuring case interview. For understanding how the case interview scoring works in candidate-led formats, see the behavioral interview consulting guide on demonstrating leadership under pressure.

Sources (checked June 17, 2026)

- Alvarez & Marsal firm overview: alvarezandmarsal.com/about-am

- A&M Corporate Finance & Restructuring practice: alvarezandmarsal.com/expertise/global-corporate-finance

- A&M on 13-week cash flow methodology: alvarezandmarsal.com/thought-leadership/the-13-week-cash-flow

- A&M firm history: alvarezandmarsal.com/our-history-bp

- Alvarez and Marsal Wikipedia: en.wikipedia.org/wiki/Alvarez_and_Marsal

- Wall Street Oasis A&M interview questions (2026): wallstreetoasis.com/company/alvarez-marsal/interview

- Hacking the Case Interview, A&M guide: hackingthecaseinterview.com/pages/alvarez-marsal-case-interview

- Management Consulted, A&M interview: managementconsulted.com/alvarez-marsal-interview

- Wall Street Prep, 13-week cash flow model: wallstreetprep.com/knowledge/demystifying-the-13-week-cash-flow-model-in-excel

- A&M campus recruiting FAQs: careers.alvarezandmarsal.com

FAQ

Frequently asked questions

Keep reading

- Expedition EY: assessment format, practice plan, and consulting prepFirm Specific · May 22, 2026

- KPMG Case Interview Guide: Format, Written Case, and Prep Strategy (2026)Firm Specific · Mar 31, 2026

- McKinsey vs BCG: 10 Real Differences (2026 Guide)Firm Specific · May 1, 2026

- Cornerstone Research Case Interview Guide: Process, Economic Analysis Cases, and Worked ExamplesFirm Specific · Apr 8, 2026